Overview1

Equity markets have experienced notable volatility in recent days and weeks as the new administration continues to execute policies related to government spending and tariffs.

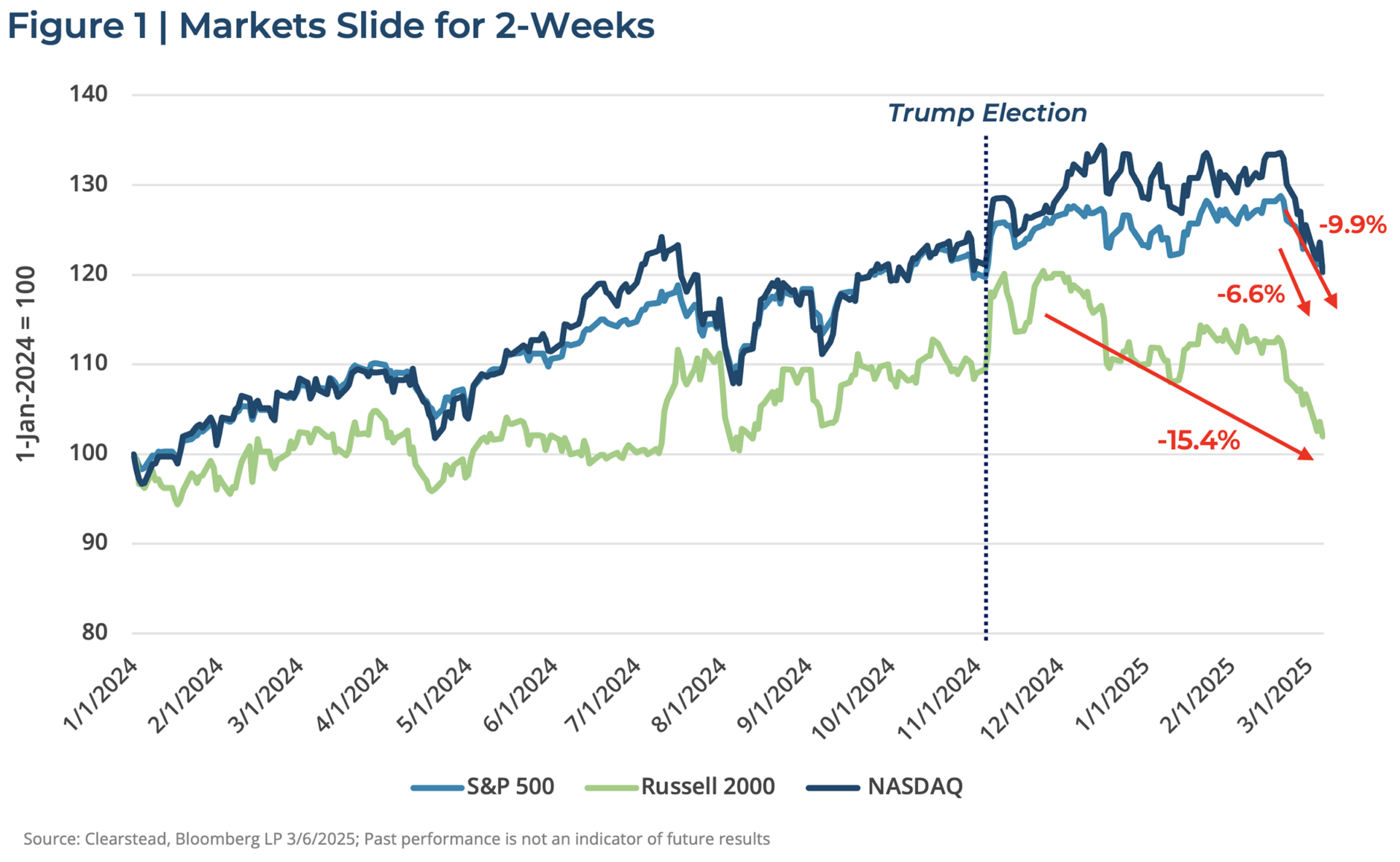

As of the close of March 6, 2025, the S&P 500 has declined -6.6% from its all-time high reached on February 19, 2025. Small cap stocks (Russell 2000 index) have declined -15.4% from its most recent peak on November 24, 2024 (see Figure 1).

Meanwhile in bond markets, the 10-year US Treasury has faced similar volatility as yields have fallen from its 2025 high of 4.79% to 4.28%—though remains in a broader trading range of 3.75% to 4.75%. High yield bond spreads have widened out modestly as equity markets have sold off, though remain well below long-term averages.

A few thoughts from us about the reasons behind the sell-off as well as near-term expectations.

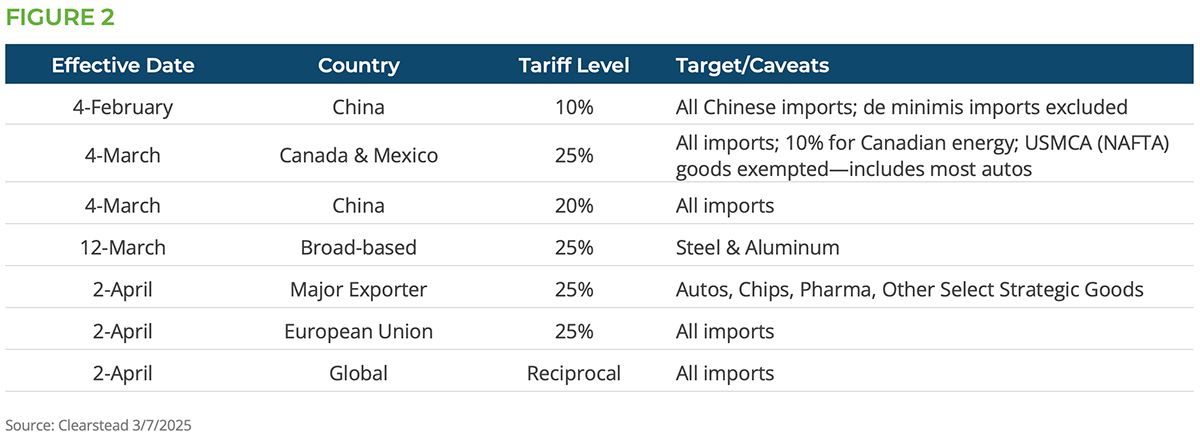

- The combination of Trump’s tariff implementation on Canada/Mexico/China along with some aspects of DOGE agenda has been the catalyst for a sell-off over the past few days, including today (see Figure 2).

- Investor sentiment in the US has taken a hit over the past few weeks, as have numerous sentiment indicators related to the US economy—such as the Conference Board, PMIs, and AAII Bull/Bear survey.

- One model of GDP growth (Atlanta Fed GDPNowcast) is suggesting sharply negative growth in Q1—as of now we do not think that is likely, but numerous indicators suggest a more cautious consumer and building evidence that the corporate sector is increasingly skittish around capital expenditures plans for spending—so expect slower growth in H1-2025 than what we anticipated pre-inauguration.

- Much of what we have seen by way of policy has been counter cyclical, though it is important to note that these are important pieces to partially fund an eventual pro-cyclical tax policy.

- Markets may have assumed that there would be a “Trump Put” (President Trump is well-known for using the S&P 500 as barometer of his economic policies) when it came to US equities, but sentiment may be shifting that the Trump administration is more willing to suffer some near-term market disruptions in order to advance their trade and tax agendas.

- We think the net of today’s headlines combined with an eventual tax bill are still likely to be pro-growth. But markets will need to navigate a volatile path until full scope of the Trump administration’s economic policies are implemented.

- Volatility is likely to remain a fixture for equity markets as they adjust to policy headlines.

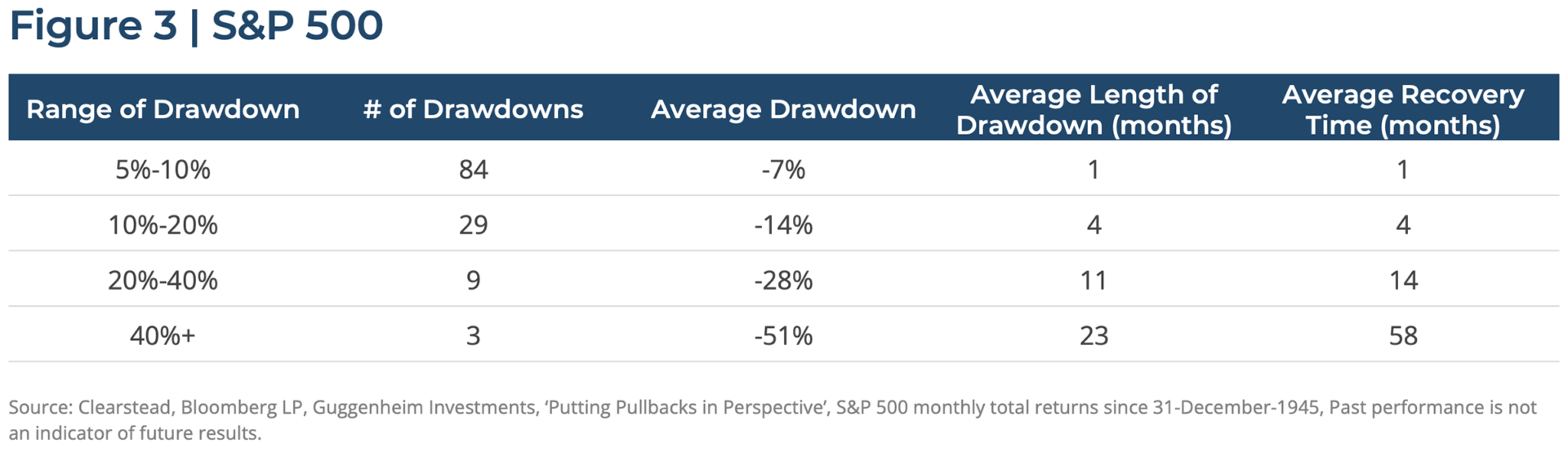

- We would like to reinforce that declines for public markets, and volatility in general, are features not bugs of markets (see Figure 3).

The Trump Administration’s economic policies are moving quickly and Clearstead is actively monitoring these developments, and we will provide additional updates as needed.

Sources

[1] Bloomberg LP as of 3/6/2025

Disclosures: Any performance data shown represents past performance. Past performance does not guarantee future returns. Current performance data may be lower or higher than the performance data presented. The information provided is intended for investors are qualified to invest in alternative investments and are willing to accept the increased risks and illiquidity for alternative investments. The information in this report is from sources believed by Clearstead Advisors, LLC (“Clearstead’) to be reliable as of the date listed or presented and is subject to change without notice. The views expressed herein are those of Clearstead investment professionals at the time comments were made, may not be reflective of their current opinions and are subject to change without notice. This material is for informational purposes only and does not consider the investment objectives or financial situation of the person receiving this information. A person seeking information about an investment strategy represented in these materials should contact a financial professional to help evaluate as to whether it is consistent with a person’s investment objectives, risk tolerance, and financial situation. The information contained herein or any opinion expressed shall NOT be construed to constitute an advertisement, investment advice, an offer to sell or a solicitation to buy any securities mentioned herein or other financial instruments. This commentary does not purport to provide any legal, tax, or accounting advice. Clearstead disclaims any liability for any direct or incidental loss incurred by applying any of the information in this report. Performance of all citied indices is on a total return basis with dividends reinvested. Benchmarks may be included for informational purposes to measure the performance of investments compared to markets in general. Clearstead is making no claim that an included benchmark is the most appropriate for evaluating an investment strategy.

Related or Tagged New Posts

market perspectives

March 16th 2026

Research Corner | 3/16/2026

market perspectives

March 9th 2026

Research Corner | 3/9/2026

market perspectives

March 2nd 2026

Impact of Escalating Conflict in Iran

market perspectives

March 2nd 2026

Research Corner | 3/2/2026

market perspectives

February 23rd 2026

Research Corner | 2/23/2026

market perspectives

February 16th 2026

Research Corner | 2/16/2026

market perspectives

February 12th 2026

Market Update | US Dollar Debasement

market perspectives

February 9th 2026

Research Corner | 2/9/2026

market perspectives

February 2nd 2026

Research Corner | 2/2/2026

market perspectives

January 26th 2026

Research Corner | 1/26/2026

market perspectives

January 20th 2026

Research Corner | 1/20/2026

market perspectives

January 12th 2026

Quarterly Market Insights | 4Q25