EQUITY MARKETS REBOUND IN Q2 AS INVESTORS LOWER NEGATIVE TAIL RISKS

“To me, consensus seems to be the process of abandoning all beliefs, principles, values and policies. So, it is something in which no one believes and to which no one objects.” – Margaret Thatcher

Summary

US economic growth rebounded in Q2 amid US policy de-escalation regarding tariffs.

The status of most US corporates and consumers remains healthy and labor markets continued to be resilient during the quarter.

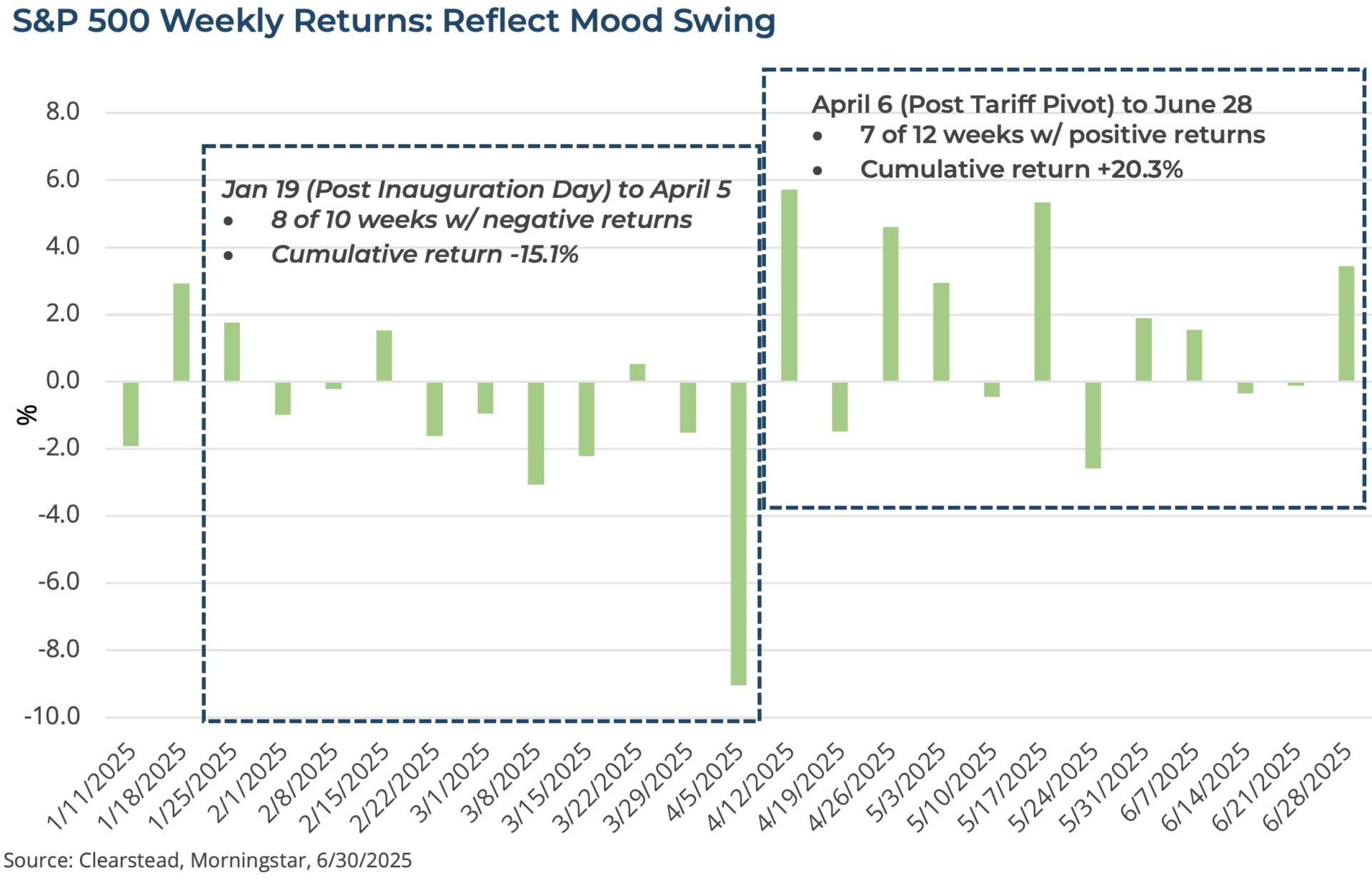

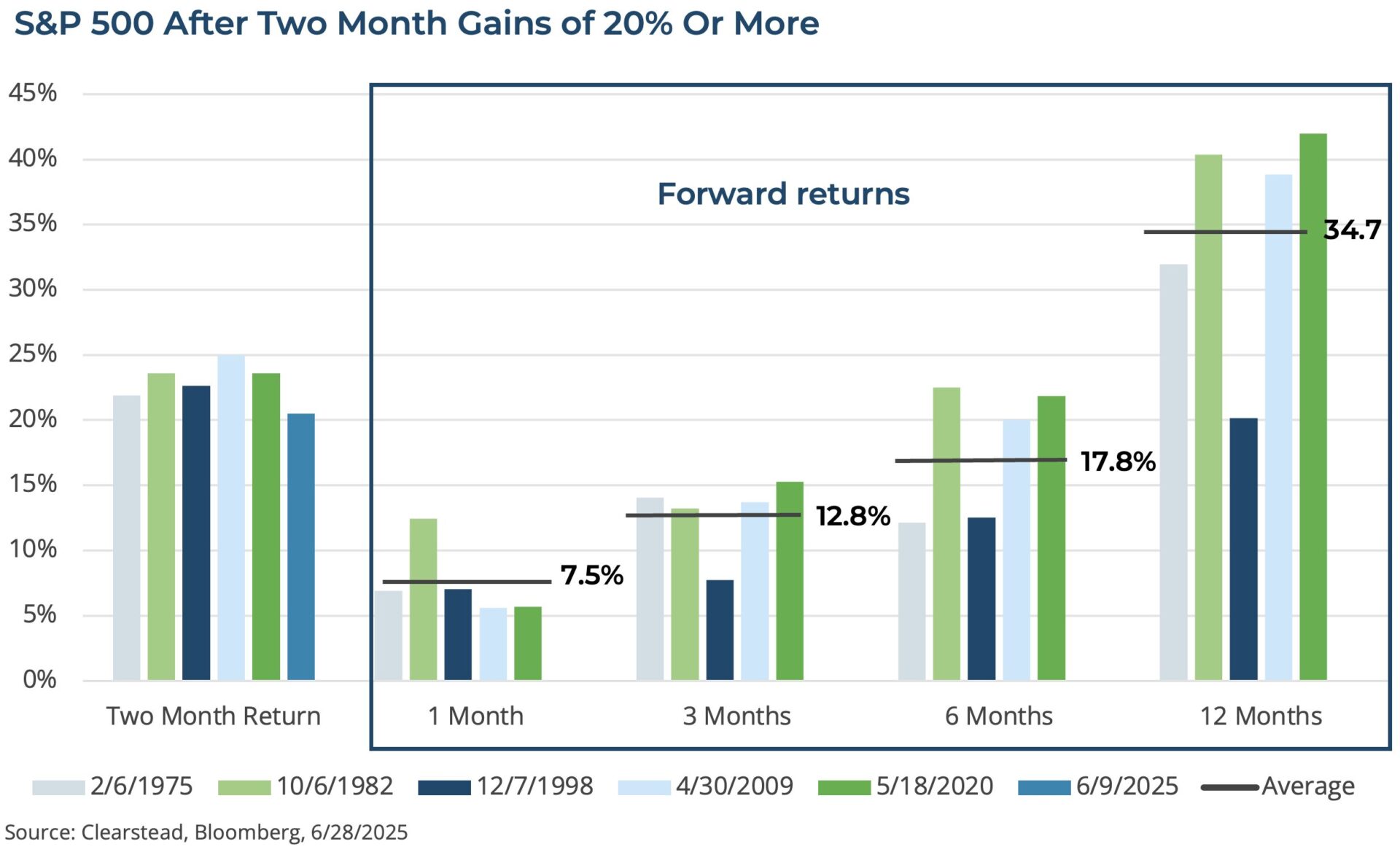

Volatility gripped markets in April but over the course of Q2 the S&P 500 rebounded from Q1’s declines and ended June at new record highs and delivering year-to-date gains.

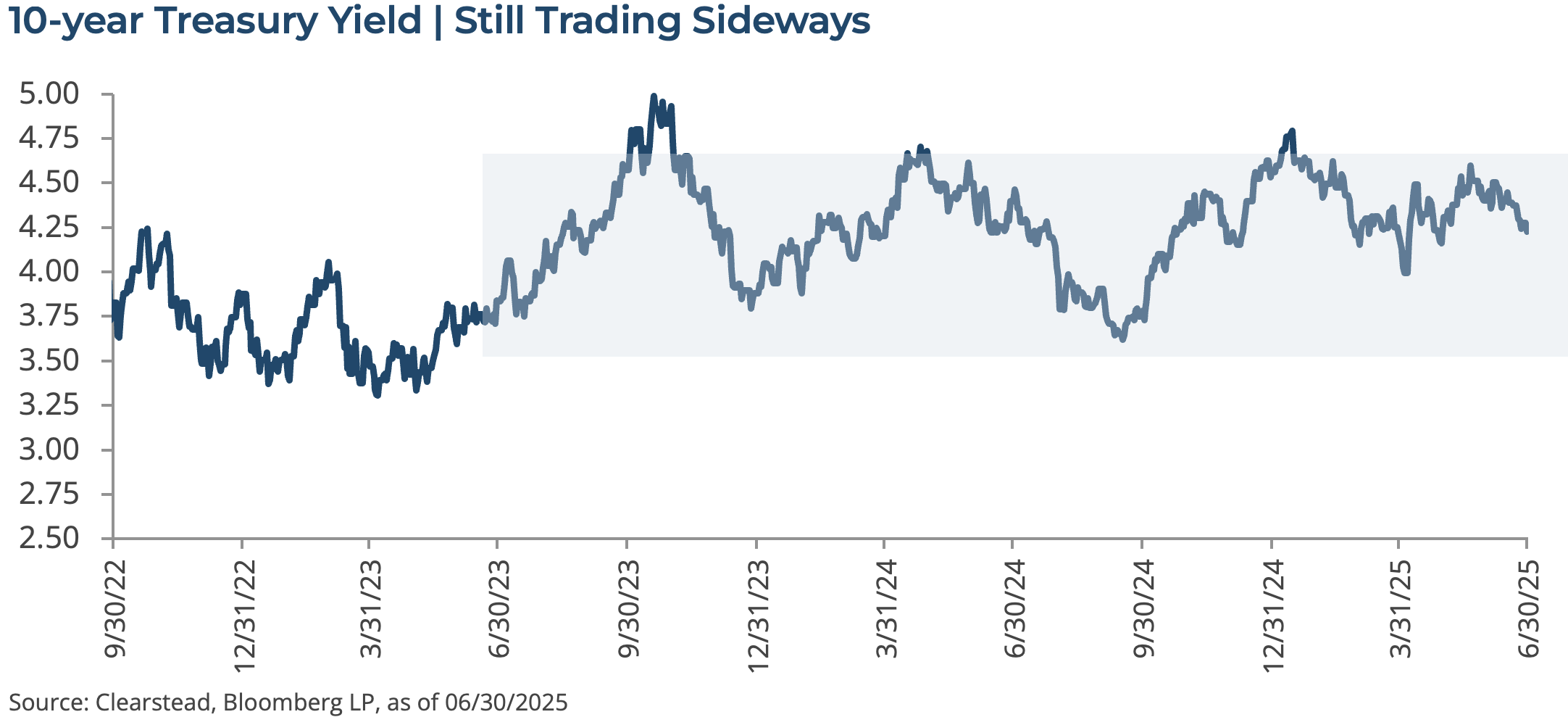

Bond markets were also volatile, but the yield on the 10-Year US Treasury ended Q2 little changed from Q1.

Despite the equity market volatility, corporate credit spreads declined, and credit markets generated positive returns.

Economy

US tariff policy pivot, resilient economy and market sentiment shift

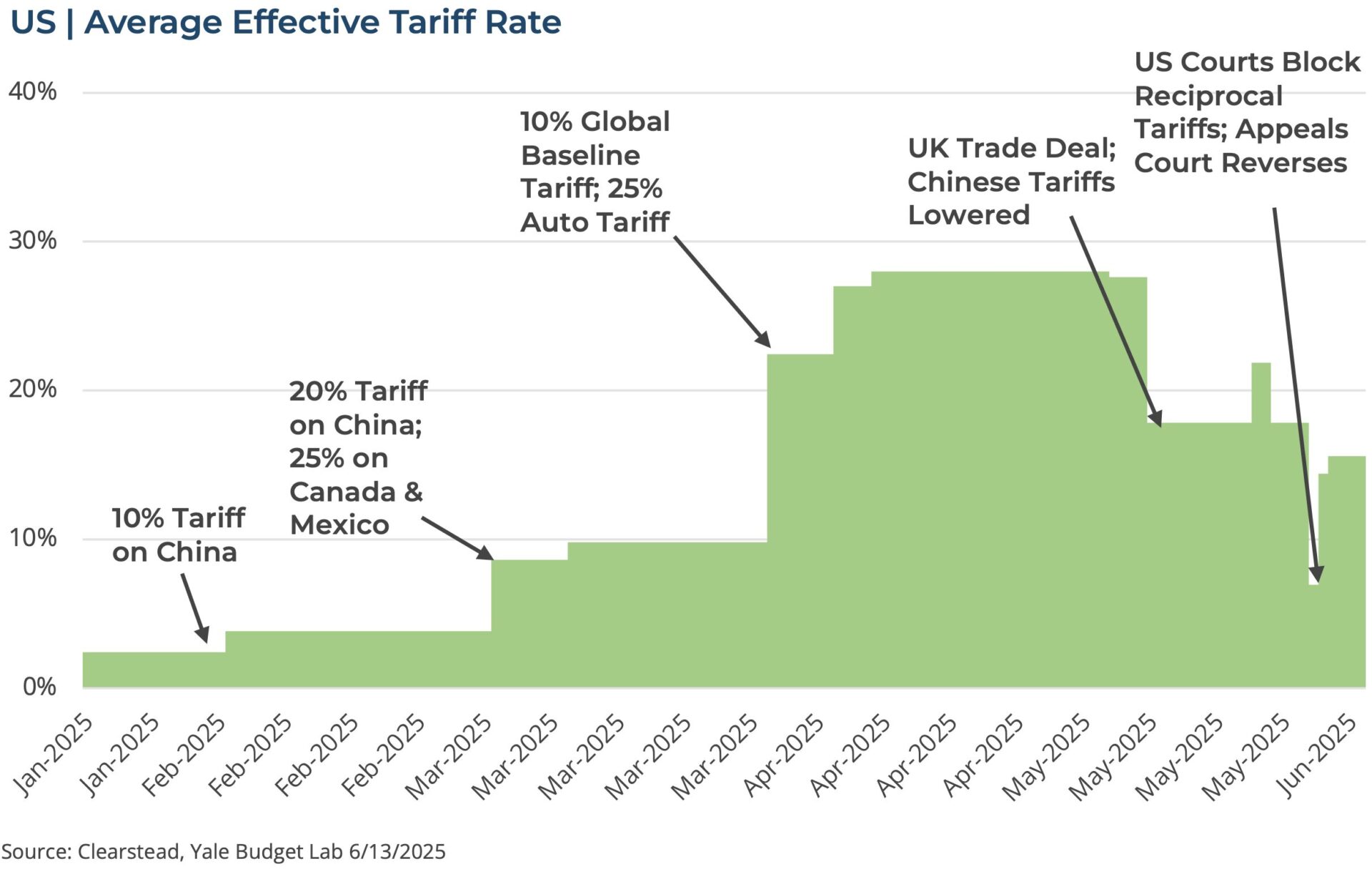

Tariffs dominated the headlines for the first half of Q2. The Trump administration announced sweeping reciprocal tariffs on April 2nd, which raised the average tariff rate for US imports to the highest levels in nearly 100 years. Despite the fact that President Trump had campaigned on raising tariffs, the breadth and magnitude of the tariffs caught financial markets off guard. Within days of the announcement, the S&P 500 had shed nearly 10%1 and briefly touched bear market territory (down nearly 20%1 from its recent peak). However, on April 8th, the Trump administration pivoted and announced a 90-day pause to most of these tariffs pending further bilateral talks. In the ensuing weeks, the Trump administration successfully negotiated a framework for a trade deal with the UK as well as some progress to deescalate the trade war with China (see Research Corner 12-May), which eased market concerns related to an all-out global trade war and the negative impact on the world economy and global corporate earnings.

In the second half of Q2, equity markets became more focused on the strong Q1 earnings season as well as economic data that seemed to be at odds with the narrative of a stalling economy and rising inflationary pressures. Q1 earnings for the S&P 500 registered over 13%2 year-over-year (YoY) growth, while Q2 expectations are for earnings growth of 5%3 YoY. For the broader economy, the Atlanta Fed’s GDP-Nowcast—a real-time measure of economic growth—currently indicates over 2.6%1 YoY growth for Q2. The labor market, the linchpin of the US consumer-oriented economy, has remained strong with unemployment steady at about 4.2%1 for the first half of the year and solid job creation—the US has averaged about 125,0001 new jobs created each month since the start of the year. Additionally, as we entered June, markets began to look forward to a sweeping new tax bill which was just signed into law that should provide some front-loaded stimulus for the US economy.

Equity Markets

Mag-7 resurgence; retail investors buy the dip; US exceptionalism?

The shift in the market’s focus from the negative tail risks related to evolving US tariff policy, which dominated Q1 and continued into the first weeks of Q2, to the strong earnings season and the rebound in AI stocks marked a sharp reversal in investor sentiment. A variety of indicators showed the negative sentiment that built up in Q1 gave way to increasing optimism in Q2. For instance, the Michigan survey of consumer sentiment increased in June for the first time in six months, the weekly bull-bear survey of individual investors increased gradually throughout the quarter, measures of retail investor flows showed that the average investor “bought the dip” during the quarter, and the VIX index—the so called Fear Guage—declined steadily from the highest levels since the COVID pandemic from early in the quarter to end June below its long-run average.

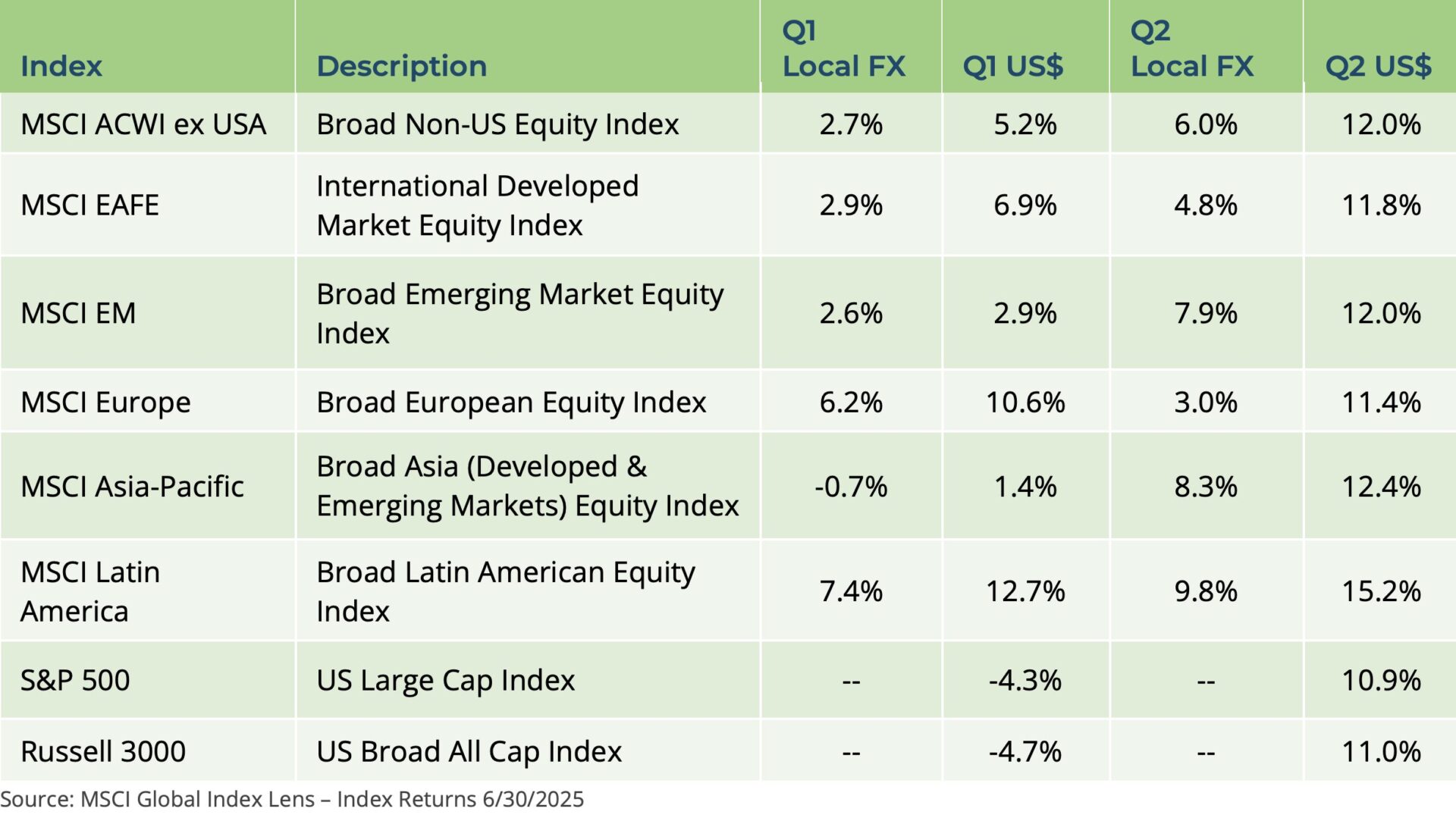

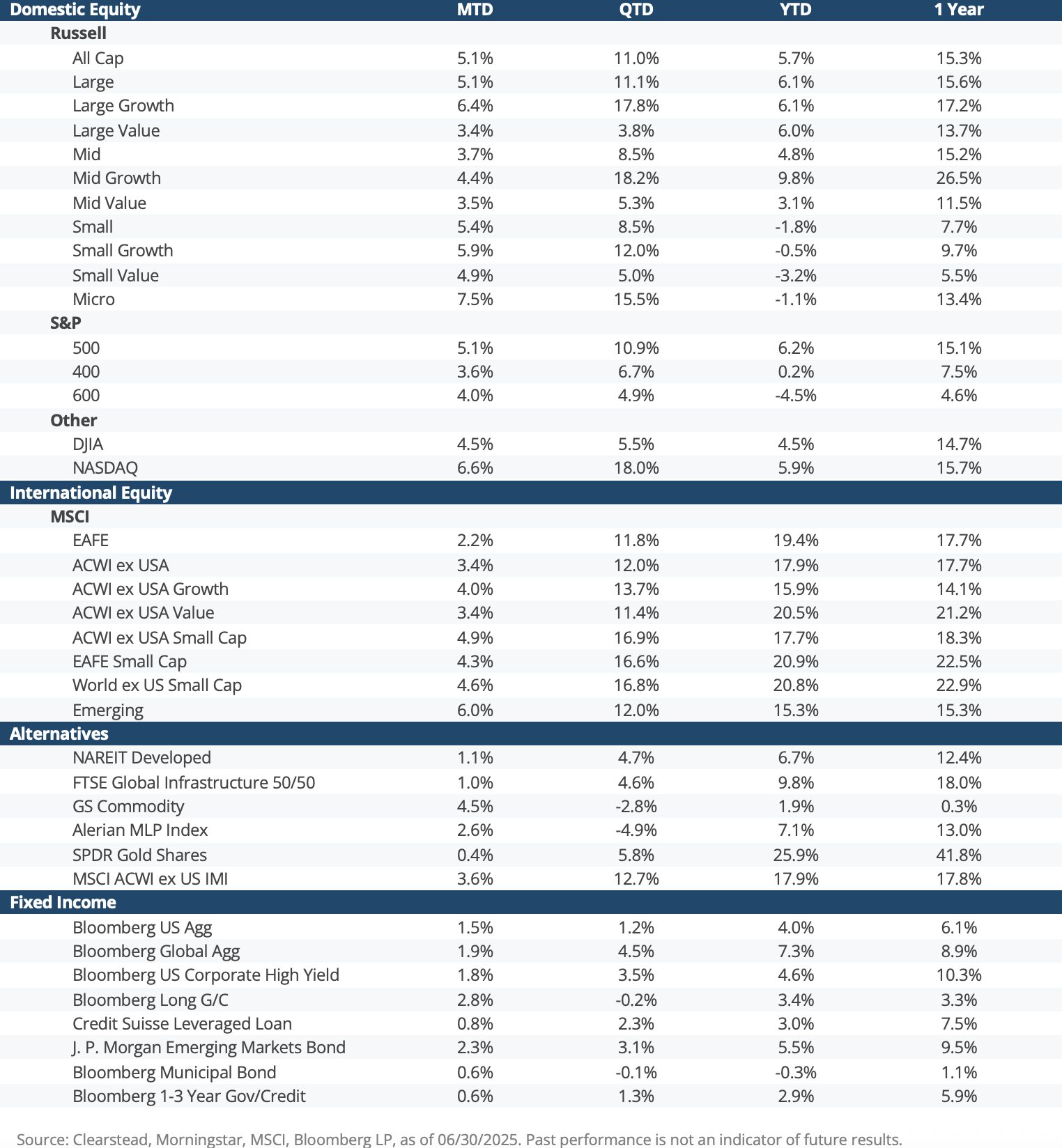

The rebound in the S&P 500 was led by the so-called Magnificent-7 (Mag-7: Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla), which rebounded on renewed enthusiasm for the AI trade. In Q1, the Mag-7 were down -16.0%1 compared to the S&P 500 ex Mag-7 which was positive 0.5%1—prompting jokes that the Mag-7 had become the Lag-7. However, in Q2 the Mag-7 shook off that moniker and gained 21.0%1 compared to the S&P 500 ex Mag-7 which gained only 7.9%1. The Mag-7 were once again powered by NVIDIA, which gained over 45.0%1 during Q2 as demand for AI semiconductors looks robust and many firms are developing industry specific AI-models to drive productivity and increase firm margins. After the strong outperformance of international equity markets in Q1, international equites performed similarly to US markets in Q2. The MSCI ACWI ex USA gained 12%1 (in US$ terms) for the quarter, which was approximately 1.0 percentage point1 better than the S&P 500. All this outperformance in Q2 can be attributed to the weakening of the US dollar. Over the course of the past three months, the US dollar slid against a basket of developed market and emerging market currencies, particularly the Euro, Japanese Yen, and South Korean Won. This movement in the dollar boosts the results for non-US equity returns for US dollar-based investors. A key question going forward remains if non-US equites will broadly outperform US equities and will any future outperformance be the result of international equity fundamentals—superior earnings, sales, margins—or simply because of a continued multi-period slide of the US dollar.

Fixed Income Markets

The short and the long of the fixed income story

It was a chaotic quarter in fixed income markets that delivered results dependent on where one stood on the yield curve. In sum, the Bloomberg US Aggregate Bond Market gained 1.2%1 in the quarter, while high yield bonds gained 3.5%1 amid tightening credit spreads. Short-term rates focused on the Federal Reserve and monetary policy. The Fed held interest rates steady and noted that they desired to see the extent to which the new tariff policy had on core-inflation before making any further adjustments to US monetary policy. Although they maintained a “wait and see” attitude, they continued to project two rate cuts by year-end. As such, short-term 2-year Treasury yields declined by 17 bps1 in Q2 (3.89% to 3.72%)1.

At the other end of the yield curve, 30-year Treasury yields rose by 19 bps1 (4.59% to 4.78%)1. Due to the “One, Big, Beautiful Bill” the markets fear the trillions added to US debt and are demanding more yield to compensate for the duration risk of long-term bonds. At the beginning of the 21st century, the total Federal government debt as a percentage of GDP was ≈ 60%; today it stands at ≈100% and is estimated to grow to 156% by 2055.4 The bond vigilantes have for years been howling about this growing mountain of debt and financial markets appear to be listening at this time.

Looking towards year-end, fixed income investors are likely to experience a roller coaster ride of interest rates rising and falling but, in the end, fully earning their coupon income in an environment where rates ended little changed from where they began.

Summary & Outlook

As we look forward to Q3, a few things become apparent. First, the consensus wisdom in the market is that the US dollar is poised for a secular decline. This argument posits that the unorthodox and, at times chaotic, changes in policy ushered in by the Trump administration related to tariffs, immigration, and multi-national security policy (US security guarantees) have spurred many foreign governments, investors, and central banks to move away from US dollar-based assets. This logic underpins the viewpoint that the US dollar is likely to weaken over the next several quarters, if not years. In short, we are not fully convinced that this thesis will play out.

For the global economic landscape, the US still seems to have the most innovative and quickly growing economy among global developed countries. The AI-boom that is blossoming in the US, so far, has not been matched by any other country. Secondarily, there does not seem to be any foreign currency that can rival the US dollar in terms of its stability, efficiency, and ubiquity. As a result, we are skeptical of the argument that calls for the dollar to structurally slide over the coming years. Nonetheless, we are watching the developments related to the US dollar and the returns of non-US risk assets, and we are evaluating options for hedging some exposure to US investments should the headwinds to the US dollar prove to be more severe than we have seen thus far.

US markets have a fair amount of positive momentum heading into the summer months. The S&P 500 closed out Q2 at a new record high, market technicals look supportive, and the Trump administration may further boost market sentiment with a new fiscal package (One Big, Beautiful Bill), which has numerous stimulative measures front-loaded over the next few years. This is not to say that US markets are in a goldilocks environment. There remains uncertainty as to the impact of the US tariff policy—will Trump increase tariffs in July absent direct bilateral deals or will the current tariff policy (current state) weaken growth, curb corporate profits, or spur inflation? The recent rally in the S&P 500 has, once again, been powered by a narrow group of AI-sector stocks (particularly the Mag 7: Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla) and the valuation for the S&P 500 is very high relative to long-run index history. Expectations for future Fed action—either cuts or an extended pause—are fluid. Therefore, as we head into Q3, equity markets have optimistic investor sentiment behind them, but they are also priced for a very positive environment in H2-2025. An unforeseen setback to AI-stock earnings, another adverse pivot on US tariffs, the failure of Congress to pass a budget bill, a Fed rate shock, or the re-emergence of a major geopolitical shock (Ukraine, Middle East, South China Sea) could reset investor expectations, and we could see equity market volatility re-assert itself in the months ahead.

[1] Bloomberg LP

[2] Factset Earnings Insight, as of 5/3/2025

[3] Factset Earnings Insight, as of 7/3/2025

[4] Congressional Budget Office, The Long-Term Budget Outlook: 2025 to 2055, March 27, 2025

DISCLOSURES

Information provided is general in nature, is provided for informational purposes only, and should not be construed as investment advice. These materials do not constitute an offer or recommendation to buy or sell securities. The views expressed by the author are based upon the data available at the time the article was written. Any such views are subject to change at any time based on market or other conditions. Clearstead disclaims any liability for any direct or incidental loss incurred by applying any of the information in this article. All investment decisions must be evaluated as to whether it is consistent with your investment objectives, risk tolerance, and financial situation. You should consult with an investment professional before making any investment decision. Performance data shown represents past performance. Past performance is not an indicator of future results. Current performance data may be lower or higher than the performance data presented. Performance data is represented by indices, which cannot be invested in directly.