OBSERVATIONS

- Markets grinded higher last week, with the S&P 500 gaining 1.1% and small caps (Russell 2000) gaining 0.7%. The yield on the 10-year Treasury increased 4 basis points to end the week at 4.09%.[1]

- The long-delayed housing starts data showed that starts increased in both November (1.322 million annualized rate) and December (1.404 million annualized rate) from October’s 1.272 million rate. However, December’s 1.4 million starts were 7.3% below the housing starts in Dec-2024, while new home sales fell in December to 745k (annualized rate)—down 1.7% from November’s new home sales figure.[1]

- The National Association of Homebuilders Housing Market Index—a gauge of the sentiment among major home builders—declined in February to 36 from January’s 37 level as homebuilders were increasingly pessimistic about sales over the next six-months and prospective buyer traffic in model homes fell.[1]

- Industrial production increased by 0.7% month-over-month (MoM)—more than expected—in January on the back of growth in both the manufacturing and utilities output. Activity in the mining sector fell slightly.[1]

- Durable goods orders fell by 1.4% MoM in December. Non-defense capital goods orders excluding aircraft -a proxy for overall fixed capital investment—increased by more than expectations to 0.6% MoM.[1]

- Initial unemployment claims declined to 206k new claims last week, which was 23k claims fewer than the week prior and about 15k fewer than the same week a year ago.[1]

- The Fed’s preferred gauge of inflation, the PCE Index, showed that inflation ticked up in December with the headline PCE index increasing to 2.9% year-over-year (YoY) from November’s 2.8% rate. Core-PCE—which excludes food and energy—increased to 3.0% YoY from November’s 2.8% rate.[1]

- The US economy grew by less than expected in Q4, with the preliminary estimate for real GDP growth registering 1.4% (annualized rate), primarily due to the government shutdown being a larger drag on growth than many expected. Of note, the Atlanta Fed’s GDPNow model predicted growth closer to 3.0%.[1]

EXPECTATIONS

- The Supreme Court struck down about 60% of the Trump administration’s tariffs last week, but the ruling provides little clarity on what comes next, as the cases were remanded back to lower courts to sort out.[1]

- The minutes from the latest January Federal Reserve meeting suggest that most Fed officials had little appetite for further reducing interest rates without seeing progress towards lower inflation. As a result, markets lowered their expectation of a rate cut in June to about 60%.[1]

- Oil prices increased last week with WTI (West Texas Intermediate Crude) hitting almost $67 per barrel, the highest price since mid-2025, as markets became increasingly worried that the US would attack Iran in the coming weeks—President Trump has given Iran about two weeks to make a deal. The US has moved naval and air force assets into the region as the US and Iran remain at loggerheads over Iran’s nuclear program, missile program, and aid to proxy terrorist groups like Hamas, Hezbollah, and the Houthis.[2]

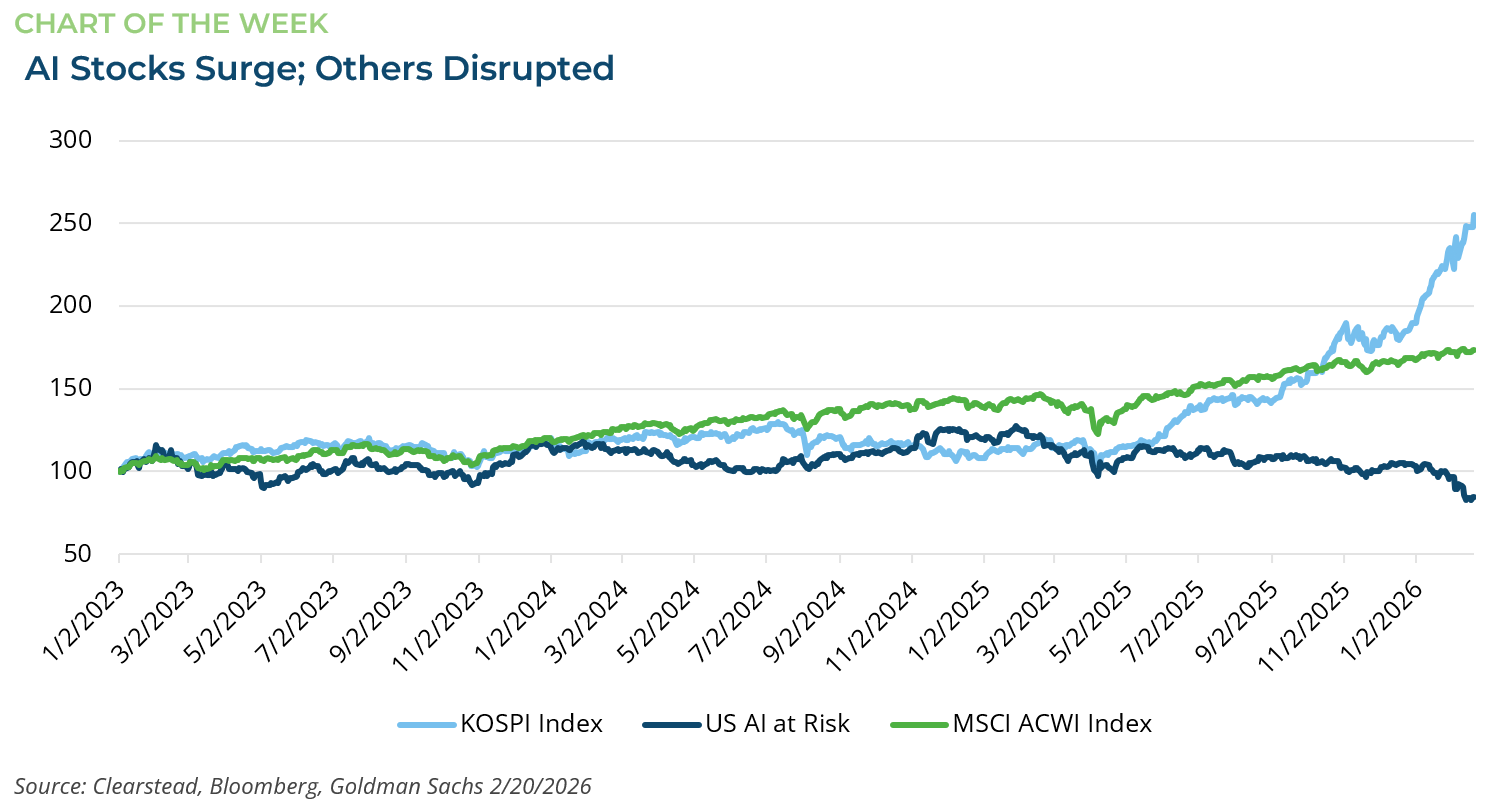

ONE MORE THOUGHT: AI Disruption – Everything, Everywhere, All at Once[1]

In recent weeks, markets have been fixated on the companies and sectors that could be severely disrupted by innovation in the AI space. In late January, a new AI model from Anthropic which aids in coding sparked a sell-off in the software sector. Today, investors continue to assess the likelihood that the sector’s profit margins and subscription-based business models might be severely disrupted by AI, both by reducing employment (the number of “seats”) and increasing efficiency as enterprises develop home-grown software solutions. In recent weeks, this angst over AI-disruption has spread to other sectors, including media, IT consulting, legal services, advertising, logistics, and financial services. In response, Goldman Sachs analysts compiled a broad basket of stocks that they judged as having a high likelihood of being disrupted – see Chart of the Week. At this time, it is unclear as to whether the market will be able to credibly assess the long-run winners and losers associated with AI, and some of the stocks recently impacted may eventually rebound. Companies like Samsung and SK Hynix—which make up approximately 40% of the Korean KOSPI Index—are seen as AI-enablers and have seen their share prices surge. At the same time, investors are increasingly rotating out of tech and into stocks exposed to a possible rebound in the US industrial cycle. If AI turns out to be as transformative as many believe, the ultimate winners may reside in the non-tech parts of the market where AI-enabled tools and robots usher in a surge in productivity, structurally higher profits, and new ways of living and operating.

[1] Bloomberg LP, 2/20/2026

[2] https://www.wsj.com/world/middle-east/u-s-gathers-the-most-air-power-in-the-mideast-since-the-2003-iraq-invasion-98ced89f?mod=article_inline

Information provided in this article is general in nature, is provided for informational purposes only, and should not be construed as investment advice. These materials do not constitute an offer or recommendation to buy or sell securities. The views expressed by the author are based upon the data available at the time the article was written. Any such views are subject to change at any time based on market or other conditions. Clearstead disclaims any liability for any direct or incidental loss incurred by applying any of the information in this article. All investment decisions must be evaluated as to whether it is consistent with your investment objectives, risk tolerance, and financial situation. You should consult with an investment professional before making any investment decision. Performance data shown represents past performance. Past performance is not an indicator of future results. Current performance data may be lower or higher than the performance data presented. Performance data is represented by indices, which cannot be invested in directly.

Related or Tagged New Posts

market perspectives

March 9th 2026

Research Corner | 3/9/2026

market perspectives

March 2nd 2026

Impact of Escalating Conflict in Iran

market perspectives

March 2nd 2026

Research Corner | 3/2/2026

market perspectives

February 16th 2026

Research Corner | 2/16/2026

market perspectives

February 12th 2026

Market Update | US Dollar Debasement

market perspectives

February 9th 2026

Research Corner | 2/9/2026

market perspectives

February 2nd 2026

Research Corner | 2/2/2026

market perspectives

January 26th 2026

Research Corner | 1/26/2026

market perspectives

January 20th 2026

Research Corner | 1/20/2026

market perspectives

January 12th 2026

Research Corner | 1/12/2026

market perspectives

January 5th 2026

Research Corner | 1/5/2026

market perspectives

December 22nd 2025

Research Corner | 12/22/2025