OBSERVATIONS

- Amid the escalating US-Iran war and surging oil prices, equity markets traded lower with the S&P 500 losing 1.6% and small caps (Russell 2000) losing 1.8%. The yield on the 10-Year Treasury rose by 14 basis points to end the week at 4.28%.[1]

- Small business optimism fell in February to 98.8, down slightly from January’s 99.3 reading, due to modest declines in hiring plans and expected sales. It remains above its long-run average of 98.[1]

- Existing home sales rose 1.7% month-over-month (MoM) to 4.09 million units (annualized rate), surpassing market forecasts.[1]

- New housing starts increased to 1.487 million units in January (latest available), which was up 7.2% MoM from December. This was well ahead of expectations of a 4.5% MoM decline.[1]

- Inflation numbers came in as expected and were little changed in February, with the headline CPI showing 2.4% year-over-year (YoY) rate. Core-CPI, which excludes food and energy, was also unchanged in February at 2.5% YoY rate.[1]

- Similarly, the PCE price index—the Fed’s preferred inflation indicator—was 2.8% YoY in February, down marginally from January’s 2.9% YoY rate. Core-PCE increased to 3.1% YoY in February from January’s 3.0% YoY figure. Both the PCE and core-PCE figures were in line with expectations.[1]

- Initial unemployment claims remain low, registering only 213k new claims last week—a 1k decrease from the week prior—and almost 8k fewer claims than the same week in 2025.[1]

- The Univ. of Michigan Consumer Sentiment index fell to 55.5 in March, down from February’s 56.6 figure, as higher oil prices and the US-Iran war weighed on sentiment.[1]

EXPECTATIONS

- The Fed meets this week, and markets expect less than a 1 percent chance of a rate cut. The rise in oil prices presents a challenge to the Fed as they increase inflationary pressures but also may induce a slowdown in global economic activity.[1]

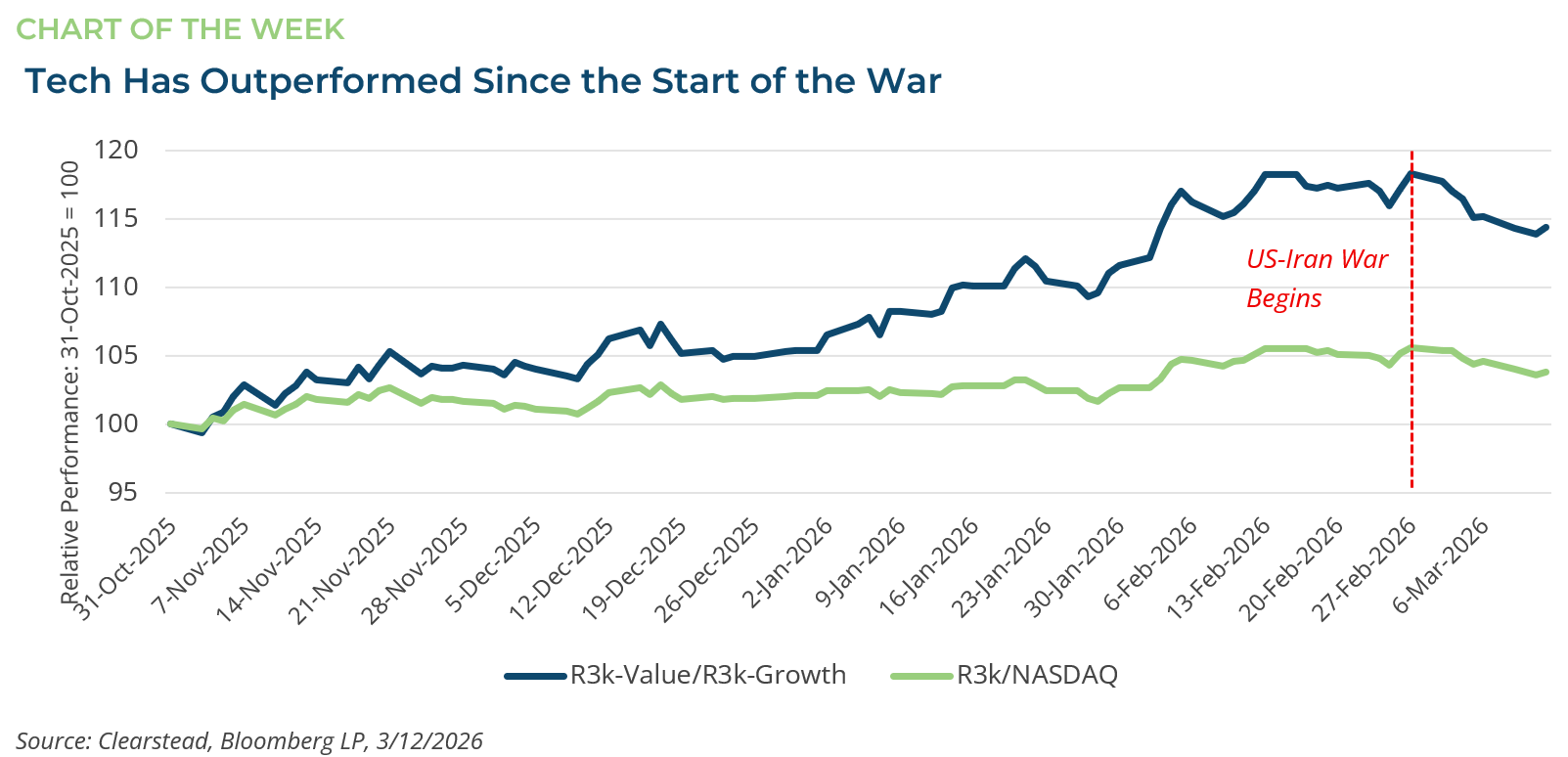

ONE MORE THOUGHT: Mega-Cap Tech Back in Favor, But Will it Last?1

For much of 2023, 2024, and 2025, the story in equity markets was one of remarkable index concentration. The Mag-7 stocks—Alphabet, Amazon, Apple, Meta, Microsoft, NVIDIA, and Tesla—and their technology-adjacent peers drove the lion’s share of returns, creating a bear market in diversification. Then, beginning in November 2025, the market suddenly shifted. The catalyst was a confluence of forces: a steepening yield curve, the Federal Reserve’s easing cycle, broadening earnings growth, a declining U.S. dollar, and an increasingly positive domestic growth narrative. Capital rotated decisively away from the mega-cap growth factor and into value, small- and mid-cap stocks, financials, industrials, and international equities. Factor leadership flipped, as low-growth, high-dividend, and cyclical factors outpaced momentum, tech, and quality-growth. The market was broadening, and breadth was celebrated as a sign of strong economic fundamentals. Now, the rotation may itself be rotating. The U.S.-Israeli military operation against Iran, which began on February 28, introduced a new variable—genuine geopolitical risk with global supply chain implications. Brent crude surged above $95 per barrel on Strait of Hormuz disruption fears, gold climbed above $5,000 per ounce, the U.S. dollar rose, and flight-to-safety trades emerged across asset classes. Cyclical and economically sensitive names and themes face headwinds from rising energy costs, potential inflationary pressure, and uncertainty. Emerging markets, particularly energy-import-dependent economies in Asia, are especially vulnerable. Counterintuitively, this risk-off environment may set the stage for large-cap technology to reassert leadership, at least for a period of time. Large-cap technology companies have fortress balance sheets and high domestic revenue exposure. These qualities look increasingly attractive as oil prices spike and the outlook for global growth remains murky. Cybersecurity, defense technology, and AI-driven government services are direct beneficiaries of an elevated threat environment. The factor picture is similarly nuanced. The quality and low-volatility factors—hallmarks of large-cap tech—tend to outperform in risk-off regimes. Momentum, which had been shifting toward value and cyclicals, may reverse. The concentration risk that drove the original rotation trade hasn’t disappeared; a different set of concerns has repriced it. Clearstead believes the initial rotation—toward smaller stocks and cyclical themes—will likely continue in 2026 absent a geopolitically driven, extended risk-off move. Broad market participation remains a healthier foundation than the hyper-concentration of prior years, and much of the fundamental case for broad-based equity gains remains intact, assuming the war ends soon. But markets are dynamic, and the factors driving leadership can shift rapidly. So long as the war continues, investors’ appetite for risk may be curtailed and the positive start to the year may not mean much.

[1] Clearstead, Bloomberg LP, 3/12/2026

Information provided in this article is general in nature, is provided for informational purposes only, and should not be construed as investment advice. These materials do not constitute an offer or recommendation to buy or sell securities. The views expressed by the author are based upon the data available at the time the article was written. Any such views are subject to change at any time based on market or other conditions. Clearstead disclaims any liability for any direct or incidental loss incurred by applying any of the information in this article. All investment decisions must be evaluated as to whether it is consistent with your investment objectives, risk tolerance, and financial situation. You should consult with an investment professional before making any investment decision. Performance data shown represents past performance. Past performance is not an indicator of future results. Current performance data may be lower or higher than the performance data presented. Performance data is represented by indices, which cannot be invested in directly.

Related or Tagged New Posts

market perspectives

April 8th 2026

Quarterly Market Insights | 1Q26 Quarterly

market perspectives

April 6th 2026

Research Corner | 4/6/2026

market perspectives

March 30th 2026

Research Corner | 3/30/2026

market perspectives

March 23rd 2026

Research Corner | 3/23/2026

market perspectives

March 9th 2026

Research Corner | 3/9/2026

market perspectives

March 2nd 2026

Impact of Escalating Conflict in Iran

market perspectives

March 2nd 2026

Research Corner | 3/2/2026

market perspectives

February 23rd 2026

Research Corner | 2/23/2026

market perspectives

February 16th 2026

Research Corner | 2/16/2026

market perspectives

February 12th 2026

Market Update | US Dollar Debasement

market perspectives

February 9th 2026

Research Corner | 2/9/2026

market perspectives

February 2nd 2026

Research Corner | 2/2/2026