OBSERVATIONS

- Markets were choppy last week but ended lower with the S&P 500 losing 0.4% and small caps (Russell 2000) losing 1.2%, while the yield on the 10-Year Treasury fell 15 basis points to end the week at 3.94%.[1]

- Housing price increases eased in December, with the Cotality S&P National Price Index falling to a 1.3% year-over-year (YoY) increase from November’s 1.4% YoY increase.[1]

- The construction spending figures for November and December were finally released last week—delayed to the 2025 government shutdown—and showed the total construction spending for 2025 was 1.4% below 2024 spending due to declines in both residential (-2.6% YoY) and nonresidential (-3.1%) construction.[1]

- Prices at the wholesale level came in higher than expected in January, with the headline PPI index falling only to 2.9% YoY, which was just below December’s 3.0% YoY rate. Meanwhile, core-PPI, which strips out food and energy prices, increased in January to 3.6% YoY prices rising from December’s 3.3% YoY figure.[1]

- Initial unemployment claims continue to be low and registered 212k new claims last week, which was 4k higher than the week prior, but nearly 27k fewer claims than the same week last year.[1]

EXPECTATIONS

- China will hold its “Two-Sessions” meetings next week, which are the annual assemblies of China’s legislature, the National People’s Congress (NPC), and the top political advisory body, the National Committee of the Chinese People’s Political Consultative Conference (CPPCC) and will layout broad economic policy goals for 2026, including an expected 2026 real GDP growth target of “4.5-5.0%”.[1]

- Many of the tariffs imposed by the Trump administration were struck down by the Supreme Court (see RC 23-Feb), but the administration imposed an across the board 10% tariff—excluding items covered under various free trade deals such as the USMCA deal—under Section 232 of the 1974 trade act. These tariffs will only last 150 days—approximately until late July—but may allow the administration the time to conduct sector specific trade analyses and then implement sector specific tariffs related to sections 201 (industry safeguarding – “dumping”) or 301 (burdens to commerce – ”trade barriers”) of the 1974 Trade Act.[1]

- NVIDIA, the largest company in the S&P 500 and the company at the center of the AI sector, reported earnings last week and beat expectations with revenue up 73% YoY and earnings up 94% YoY. Meanwhile, with NVIDIA’s earnings released, about 96% of S&P 500 have reported Q4-2025 earnings and 73% of reporting companies have had a positive earnings surprise, which is below the 5-year (78%) and 10-year (76%) average for beats. Overall, Q4 earnings are set to increase an impressive 14.2% YoY.[2]

ONE MORE THOUGHT: February’s Rotations, Dispersions, and Sell-offs – Oh My[1]

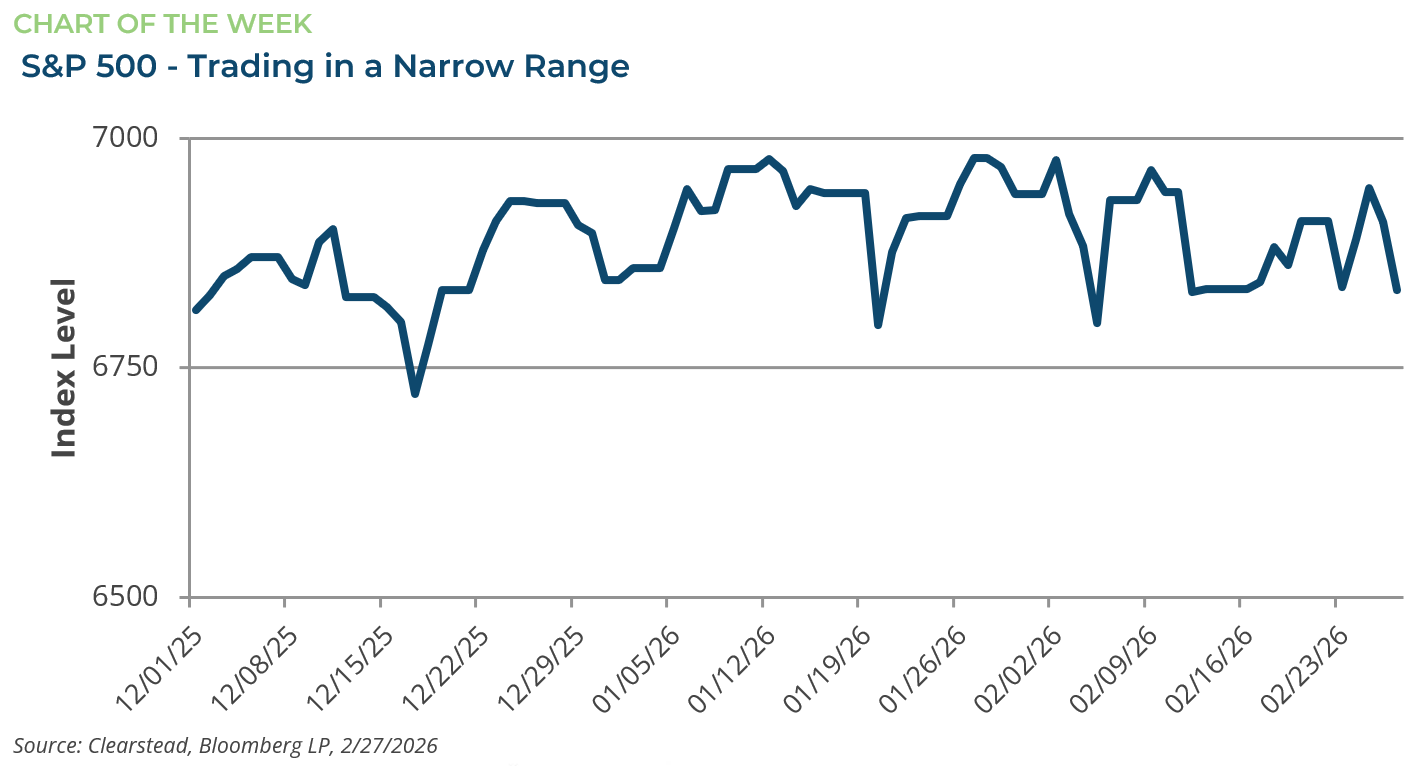

February was a month of dispersion and contrasts. The S&P 500 fell by -0.8% in February, while the equal-weight S&P and international markets (MSCI ACWI ex US) rose by 3.6% and 5.0%, respectively. Since December 1, 2025, the S&P 500 has traded between roughly 6,750 and 6,980 on a closing basis, a tight 3.4% trading range—see Chart of the Week. Despite a muted headline return, there was a tremendous amount of activity beneath the surface as investors digested the latest wave of AI disruption fears and market gains continued to broaden out to the non-tech parts of the equity market. However, performance dispersion was also particularly notable within the Technology sector, with memory names like Sandisk (SNDK) rising by 10.3% while financial software stock Intuit (INTU) fell by 18.0%. The Mag-7—Alphabet, Amazon, Apple, Meta, Microsoft, NVIDIA, and Tesla—continued to lag the market in February, declining by -7.3%. This handful of mega-cap AI beneficiaries is no longer the sole driver of global index returns, as market breadth improves and cyclical sectors, smaller-cap asset classes, and foreign stocks lead. Investors are increasingly turning to and rewarding cash-flow generators, dividend payers, and cyclical themes rather than speculative growth stocks. February was bright for international equity markets, with developed (MSCI EAFE Index) and emerging markets (MSCI EM Index) rising by 4.6% and 5.5%, respectively, even as the US dollar gained modestly against a broad range of mostly developed-market foreign currencies. South Korea stood out again in February with its equity market (MSCI Korea Index) surging by over 22.6% in dollar terms. US interest rates declined in February as investors concerned about the disruptive nature of AI, the growing tensions between the US and Iran, and the press’s obsession with potential problems in private credit turned many investors towards Treasuries in a flight to safety. The US Treasury 10-year yield declined from 4.24% to 3.94%, the 30 basis points decline was similar across the yield curve for Treasuries from 5 to 30 years.

[1] Bloomberg LP, 2/27/2026

[2] FactSet Earnings Insight 2/27/2026

Information provided in this article is general in nature, is provided for informational purposes only, and should not be construed as investment advice. These materials do not constitute an offer or recommendation to buy or sell securities. The views expressed by the author are based upon the data available at the time the article was written. Any such views are subject to change at any time based on market or other conditions. Clearstead disclaims any liability for any direct or incidental loss incurred by applying any of the information in this article. All investment decisions must be evaluated as to whether it is consistent with your investment objectives, risk tolerance, and financial situation. You should consult with an investment professional before making any investment decision. Performance data shown represents past performance. Past performance is not an indicator of future results. Current performance data may be lower or higher than the performance data presented. Performance data is represented by indices, which cannot be invested in directly.

Related or Tagged New Posts

market perspectives

March 23rd 2026

Research Corner | 3/23/2026

market perspectives

March 16th 2026

Research Corner | 3/16/2026

market perspectives

March 9th 2026

Research Corner | 3/9/2026

market perspectives

March 2nd 2026

Impact of Escalating Conflict in Iran

market perspectives

February 23rd 2026

Research Corner | 2/23/2026

market perspectives

February 16th 2026

Research Corner | 2/16/2026

market perspectives

February 12th 2026

Market Update | US Dollar Debasement

market perspectives

February 9th 2026

Research Corner | 2/9/2026

market perspectives

February 2nd 2026

Research Corner | 2/2/2026

market perspectives

January 26th 2026

Research Corner | 1/26/2026

market perspectives

January 20th 2026

Research Corner | 1/20/2026

market perspectives

January 12th 2026

Research Corner | 1/12/2026