OBSERVATIONS

- Markets traded lower again last week as the US-Iran war grinds on. The S&P 500 lost 1.9% and small caps (Russell 2000) lost 1.7%, while the yield on the 10-year Treasury rose 10 basis points to close at 4.38%.[1]

- Industrial production increased by 0.2% month-over-month (MoM) in February, better than expected, but below January’s 0.7% MoM increase. Capacity utilization was 76.3% in February, unchanged from January, but approximately 3 percentage points below its 50-year average.[1]

- The Home Builder Confidence index rose one point to 38 in March from February, driven primarily by an increase in expected sales over the next six months as well as a rise in foot traffic of potential buyers at model homes in recent weeks.[1]

- Prices at the wholesale level increased more than expected in February, with the headline PPI index increasing to 3.4% year-over-year (YoY) from January’s 2.9% YoY figure. Meanwhile, core-PPI, which excludes the volatile food and energy categories, increased to 3.9% YoY in February from January’s 3.5% YoY rate.[1]

- Initial unemployment claims remain very low, registering only 205k new claims last week which were 16k fewer claims than the week prior and 17k fewer claims than the same week last year.[1]

- New home sales fell in January to 587k (annualized rate), a 17.6% decline from December’s 712k new home sales rate. This was the lowest new home sales figure since Oct-2022.[1]

EXPECTATIONS

- President Trump announced last week that he was postponing his late March trip to Beijing as the ongoing war with Iran preoccupies US foreign policy initiatives, delaying efforts to ease frictions between Washington and Beijing over Taiwan, tariffs, computer chips, illegal drugs, rare earths, and agriculture.[2]

- In addition to the US Federal Reserve (see One More Thought), more than a dozen central banks met last week, including the Bank of Japan, the European Central Bank, the Bank of Canada, and the Bank of England. All held rates steady as the US-Iran war and the rise of oil prices have muddied their outlooks.[1]

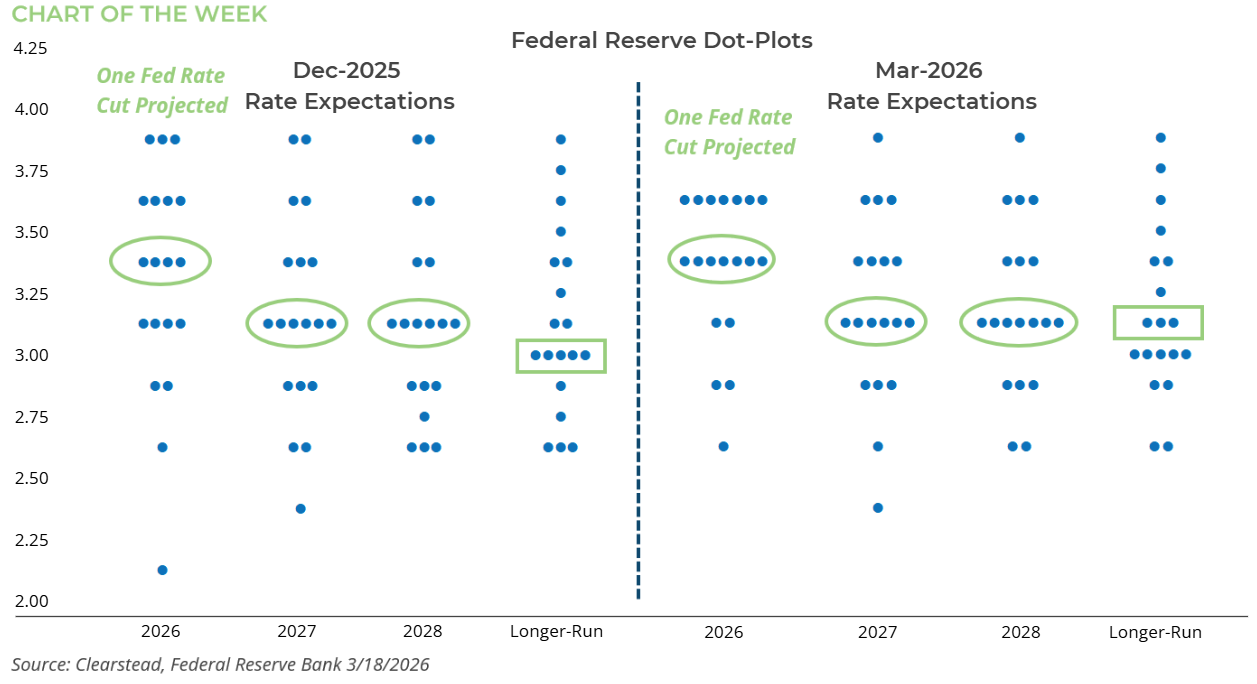

ONE MORE THOUGHT: US Federal Reserve Keeps Rates Steady[1]

Last week, the US Federal Reserve voted to keep the federal funds rate unchanged within the target range of 3.50%–3.75%. This marks the second consecutive meeting the Fed has maintained its last quarter-point rate cut in December 2025. The Fed noted that economic activity was stable, with resilient consumer spending and business investment, but housing activity remained weak. Chairman Powell acknowledged that recent job gains were low, but that the unemployment rate had largely stabilized in a relatively healthy range of 4.0% to 4.5%. Powell stated that inflation remained higher than the Fed’s target, and that most Fed participants modestly raised their expectations for inflation this year. He also emphasized heightened uncertainty on the outlook, given the war in the Middle East and the recent rise in oil prices. Powell noted that the increase in oil prices could temporarily elevate inflation readings in the coming months—a potential transitory price shock—but that the Fed was highly attuned to the potential for higher energy prices to upend longer-run inflation expectations. Powell raised the possibility that, after several years of inflation above the Fed’s 2% target, a short-term rise in prices could impact consumer expectations about future inflation. As such, the Fed would continue in wait-and-see mode until the full impact of the rise in oil prices became clearer. The Fed’s “dot-plot” projections continue to show the median participant anticipates at least one rate cut in 2026—see Chart of the Week. However, compared to the Fed’s projections from December, there is less dispersion of opinion compared to the beginning of the year. Today, there is consensus that, at most, one rate cut in 2026 is warranted. As a result, the market has dramatically adjusted its expectations for Fed action for the rest of the year. As recently as mid-February, the Dec-2026 Fed Funds Futures priced in at least two 25 basis point rate cuts and a 50% probability of a third. However, by the end of last week, the probability of any rate cuts in 2026 had dropped to 0%. Kevin Warsh has been nominated to replace Powell as the head of the Fed and, in recent weeks, has spoken publicly about the idea that the Fed might look to buttress economic growth by cutting rates in 2026. Notably, the Fed’s dot-plot chart suggests that many on the Fed’s policy committee feel differently. Warsh is expected to be confirmed before the Fed’s June policy meeting, and unless the labor market shows material weakness over the coming months or Warsh changes his view, we could see a policy clash brewing at the Fed this summer.

[1] Clearstead, Bloomberg LP, 3/20/2026

[2] https://www.wsj.com/world/china/in-delaying-china-summit-trump-faces-a-familiar-mideast-distraction-86089d2c?mod=Searchresults&pos=1&page=1

Information provided in this article is general in nature, is provided for informational purposes only, and should not be construed as investment advice. These materials do not constitute an offer or recommendation to buy or sell securities. The views expressed by the author are based upon the data available at the time the article was written. Any such views are subject to change at any time based on market or other conditions. Clearstead disclaims any liability for any direct or incidental loss incurred by applying any of the information in this article. All investment decisions must be evaluated as to whether it is consistent with your investment objectives, risk tolerance, and financial situation. You should consult with an investment professional before making any investment decision. Performance data shown represents past performance. Past performance is not an indicator of future results. Current performance data may be lower or higher than the performance data presented. Performance data is represented by indices, which cannot be invested in directly.

Related or Tagged New Posts

market perspectives

April 13th 2026

Research Corner | 4/13/2026

market perspectives

April 8th 2026

Quarterly Market Insights | 1Q26 Quarterly

market perspectives

April 6th 2026

Research Corner | 4/6/2026

market perspectives

March 30th 2026

Research Corner | 3/30/2026

market perspectives

March 16th 2026

Research Corner | 3/16/2026

market perspectives

March 9th 2026

Research Corner | 3/9/2026

market perspectives

March 2nd 2026

Impact of Escalating Conflict in Iran

market perspectives

March 2nd 2026

Research Corner | 3/2/2026

market perspectives

February 23rd 2026

Research Corner | 2/23/2026

market perspectives

February 16th 2026

Research Corner | 2/16/2026

market perspectives

February 12th 2026

Market Update | US Dollar Debasement

market perspectives

February 9th 2026

Research Corner | 2/9/2026