Observations

- Markets traded lower last week with the S&P 500 losing -1.5% and small caps (Russell 2000) falling -1.6% and the yield on the 10-year Treasury was unchanged ending the the week at 4.25%.[1]

- The S&P CoreLogic Case-Shiller U.S. National Home Price Index showed that home prices increased by 4.1% year-over-year (YoY) in January, up from December’s 4.0% YoY figure.[1]

- New home sales rebounded in February to 676k (annualized rate) from January’s 664k figure. Compared to Feb-2024, new home sales were up +5.1% YoY.[1]

- Durable goods orders increased 0.9% month-over-month (MoM), well ahead of expectations which were for a MoM decline.[1]

- Initial unemployment claims remain low and fell to 224k from the week prior’s revised level of 225k claims.[1]

- The Fed’s preferred inflation measure, the PCE index, showed that headline inflation came in as expected in February at 2.5% YoY. But core-PCE—which removes food and energy—came in higher than expected at 2.8% YoY (versus expectations for 2.7%) and January’s core-PCE was revised higher to 2.7% YoY.[1]

Expectations

- The final estimate for GDP growth in Q4-2024 was 2.4% YoY—just +0.1% YoY higher than earlier estimates for the quarter—and for the full year (2024) real GDP growth was 2.8% YoY. However, expectations for Q1-2025 have softened with the Atlanta Fed’s GDP Nowcast model (adjusted for gold imports) now showing an estimate for a -0.5% YoY decline in growth for the quarter.[1]

- President Trump announced sweeping automobile tariffs last week of 25% on autos that are imported from abroad including Mexico and Canada. The new tariffs cover autos and auto components, but currently exempt imported auto parts from Mexico and Canada covered under the USMCA trade agreement.[1]

- The Trump Administration will begin announcing reciprocal tariffs next week which are likely to be the final phase of Trump’s higher tariff initiative. The tariffs announced over the next few days or weeks will likely inform Congress of likely tariff revenue that can be expected in fiscal year 2026 and help guide lawmakers as they grapple with plans to extend the 2017 Trump-era tax cuts as well as reign in government spending.[1]

ONE MORE THOUGHT: Hard Data Sending Different Messages than Soft Data[1]

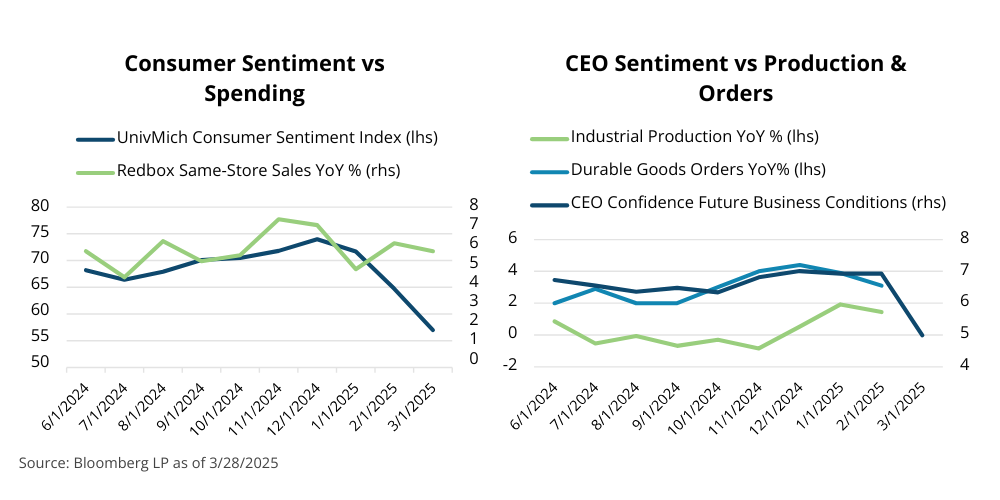

Signals of pessimism has been sweeping many parts of the US economy and financial markets, but while a variety of sentiment indicators are increasingly bearish on the direction of the economy, hard data indicators that directly relate to actual consumer spending, industrial production, and many parts of the financial markets suggest that both US economy and markets are stable. Recent examples of deteriorating sentiment include a variety of consumer confidence and sentiment indicators, the most prominent are tracked by the University of Michigan and the Conference Board, which both weakened in recent months. In the business world, CEO and purchasing manager surveys—the most popular by the ISM and Markit groups—for both the manufacturing and service sectors also have shown weakness in activity. Lastly, in terms of financial markets the S&P 500 recently declined by more than -10% from its all-time high and several market sentiment indicators—such as the AAII Bull-Bear survey—have shown bearish sentiment creeping into investors’ outlooks. However, while these sentiment indicators are sometimes viewed as being forward looking and foreshadowing of things to come, thus far, data that tracks the US consumer, US businesses, and other, less followed parts of the market, continue to show relative strength. For instance, retail sales—sometimes criticized as a lagging indicator—shows more than 3% YoY growth in both January and February. Other, more frequent measures of consumer activity such as the weekly Redbox same-store retail sales figures show no dip in consumer activity through the third week of March. Similarly, the CEO of Bank of America—the nation’s second largest bank—recently gave an interview where he noted that consumers profess to be pessimistic about the economy, but they do not seem to be changing their spending habits as judged by their proprietary credit and debit card data. In the business world, both industrial production figures from the first two months as well as recent durable goods orders suggest that businesses continue to produce, build, spend and invest. Lastly, the recent sell-off in the S&P 500 has been making headlines for much of the past several weeks, but it is worth noting two items. First, outside the Mag-7 stocks (NVIDIA, Tesla, Microsoft, Amazon, Google, Meta, and Apple) which have declined -15.7% year-to-date (YTD), most other S&P stocks are faring much better. The equal-weighted S&P 500 Index is down only -1.4% YTD and the S&P 500 excluding the Mag-7 stocks is down -0.3% YTD. Additionally, at the index level we have seen modest levels of above-trend insider buying, which typically suggests company executives are bullish on their company’s stock. Sometimes deteriorating sentiment and building pessimism portends darker days ahead for economic activity and stock market performance, but at other times it is simply a passing mood swing that improves as uncertainty and other sources of angst are removed. It is likely that April’s hard data reports will tell if the current vibe-shift seen in the surveys is indeed a harbinger of a coming economic tempest.

Chart of the Week

[1] Bloomberg LP

Information provided in this article is general in nature, is provided for informational purposes only, and should not be construed as investment advice. These materials do not constitute an offer or recommendation to buy or sell securities. The views expressed by the author are based upon the data available at the time the article was written. Any such views are subject to change at any time based on market or other conditions. Clearstead disclaims any liability for any direct or incidental loss incurred by applying any of the information in this article. All investment decisions must be evaluated as to whether it is consistent with your investment objectives, risk tolerance, and financial situation. You should consult with an investment professional before making any investment decision. Performance data shown represents past performance. Past performance is not an indicator of future results. Current performance data may be lower or higher than the performance data presented. Performance data is represented by indices, which cannot be invested in directly.

Related or Tagged New Posts

market perspectives

March 16th 2026

Research Corner | 3/16/2026

market perspectives

March 9th 2026

Research Corner | 3/9/2026

market perspectives

March 2nd 2026

Impact of Escalating Conflict in Iran

market perspectives

March 2nd 2026

Research Corner | 3/2/2026

market perspectives

February 23rd 2026

Research Corner | 2/23/2026

market perspectives

February 16th 2026

Research Corner | 2/16/2026

market perspectives

February 12th 2026

Market Update | US Dollar Debasement

market perspectives

February 9th 2026

Research Corner | 2/9/2026

market perspectives

February 2nd 2026

Research Corner | 2/2/2026

market perspectives

January 26th 2026

Research Corner | 1/26/2026

market perspectives

January 20th 2026

Research Corner | 1/20/2026

market perspectives

January 12th 2026

Quarterly Market Insights | 4Q25