OBSERVATIONS

- Markets traded higher last week following the announcement of the cease-fire deal. The S&P 500 gained 3.6%, small caps (Russell 2000) gained 4.0%, and the yield on the 10-year Treasury fell 3 basis points to end the week at 4.32%.[1]

- The ISM services index remained in economic expansion territory at 54.0, modestly below expectations of 54.9. Notably, the prices paid sub-index jumped to 70.7 (versus an expected 67.0), the highest reading since October 2022, amid the Middle East conflict. The 7.7-point jump from the prior month was the largest month-over-month (MoM) increase since the summer of 2012.[1]

- The University of Michigan Consumer Sentiment Index fell to 47.6, an all-time low. Importantly, 98% of interviews used for this survey-based index were conducted before April 7’s cease-fire announcement.[2]

- Inflation, as measured by the CPI index, jumped 0.9% in March on a MoM basis while rising to 3.3% year-over-year (YoY). Core inflation, which excludes more volatile food and energy, rose 0.2% MoM and 2.6% YoY. The energy component alone rose +10.9% in March reflecting the rise in oil and gas prices.[1]

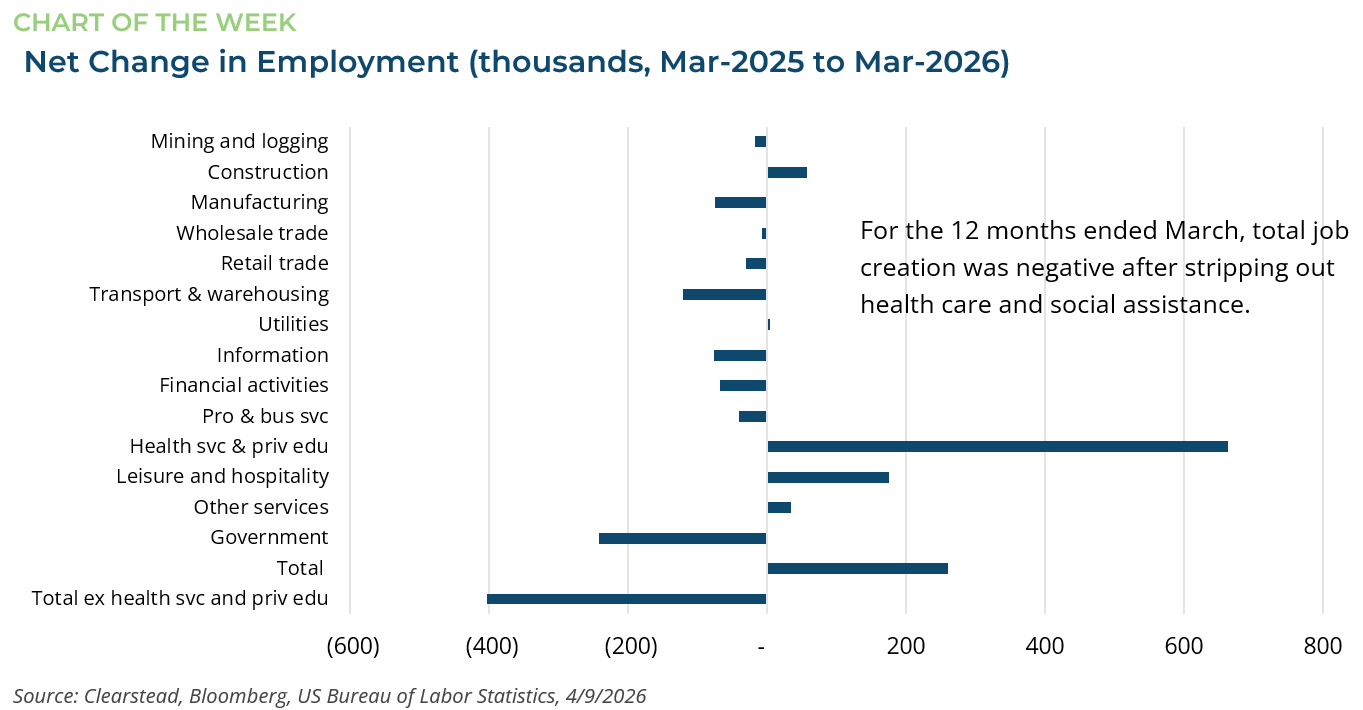

- Initial jobless claims came in at 219k, slightly above expectations of 210k. The four-week moving average remains very low at 209.5k. While claims remain relatively low, there are nuances to overall job creation worth highlighting — see One More Thought.[1]

- Fourth quarter 2025 final GDP data showed the economy grew at an annualized pace of 0.5%, below expectations of 0.7%. The Bureau of Economic Analysis estimates that the government shutdown reduced GDP by one full percentage point in Q4.[3]

EXPECTATIONS

- Minutes from the Federal Reserve’s March meeting suggested that some officials see scope for rate hikes if inflation remains above target. Even so, markets still largely expect no further increases this year and future rate decisions will depend on incoming data, including the war’s effects on energy prices and inflation, amid signs of underlying shifts in the labor market.[1]

- Earnings season will kick off soon, with the highest number of S&P 500 companies issuing positive earnings guidance in five years heading into the season. For the first quarter, earnings growth is expected to be 12.6% YoY, which would mark the sixth consecutive quarter of double-digit earnings growth for the index.[4]

ONE MORE THOUGHT: The Narrowing US Job Market[5]

Rick Rieder of BlackRock (a recent Federal Reserve Chair nominee) recently observed that inflation, while still somewhat sticky above the Federal Reserve’s 2% target, no longer appears to be the primary macro risk. Instead, he argues that labor market weakening is becoming the more important concern in the months ahead. Weekly unemployment claims remain relatively benign, and the 4.3% unemployment rate is not yet alarming. Still, there are signs of softening beneath the surface. Wage growth has moderated, average hours worked have edged lower, and labor force participation has declined as some would-be workers exit the labor market—although some of this is related to demographic shifts. The weakness is also more pronounced among younger workers, with the 20–24 age cohort now showing an unemployment rate of 8.2% and most of this is concentrated in those with a bachelor’s degree or higher. What stands out most is the narrowness of job creation. Over the past year, nearly all net job growth has come from healthcare, while most other areas of the private sector have contributed little on balance. In fact, excluding healthcare, the labor market has effectively posted negative job growth over the last twelve months through March 2026 (Chart of the Week). Leisure and hospitality have been adding jobs at a moderate pace and construction continues to add jobs despite weakness in housing and commercial real estate, while all other categories appear softer. The latest ISM Services PMI adds to the cautious tone: its employment index came in at 45.2%, signaling contraction rather than expansion. It is highly unusual to have job growth concentrated in limited sectors while the economy continues to grow at the pace with which it has. Similarly, we have never seen the unemployment rate remain stable despite so few net jobs created over the past year. Overall, the labor market is in a unique equilibrium—one not seen ever in the past 75 years—and it is something we will continue to monitor closely.

[1] Bloomberg LP, 4/3/2026

[2] https://www.sca.isr.umich.edu/, 4/10/2026

[3] BEA, as of 4/9/2026

[4] FactSet Earnings Insight 4/10/2026

[5] Bloomberg LP, Blackrock Fixed Income Outlook, Q1 2026

Information provided in this article is general in nature, is provided for informational purposes only, and should not be construed as investment advice. These materials do not constitute an offer or recommendation to buy or sell securities. The views expressed by the author are based upon the data available at the time the article was written. Any such views are subject to change at any time based on market or other conditions. Clearstead disclaims any liability for any direct or incidental loss incurred by applying any of the information in this article. All investment decisions must be evaluated as to whether it is consistent with your investment objectives, risk tolerance, and financial situation. You should consult with an investment professional before making any investment decision. Performance data shown represents past performance. Past performance is not an indicator of future results. Current performance data may be lower or higher than the performance data presented. Performance data is represented by indices, which cannot be invested in directly.

Related or Tagged New Posts

market perspectives

April 8th 2026

Quarterly Market Insights | 1Q26 Quarterly

market perspectives

April 6th 2026

Research Corner | 4/6/2026

market perspectives

March 30th 2026

Research Corner | 3/30/2026

market perspectives

March 23rd 2026

Research Corner | 3/23/2026

market perspectives

March 16th 2026

Research Corner | 3/16/2026

market perspectives

March 9th 2026

Research Corner | 3/9/2026

market perspectives

March 2nd 2026

Impact of Escalating Conflict in Iran

market perspectives

March 2nd 2026

Research Corner | 3/2/2026

market perspectives

February 23rd 2026

Research Corner | 2/23/2026

market perspectives

February 16th 2026

Research Corner | 2/16/2026

market perspectives

February 12th 2026

Market Update | US Dollar Debasement

market perspectives

February 9th 2026

Research Corner | 2/9/2026