OBSERVATIONS

- Markets traded higher last week as investors perceived a higher likelihood of a de-escalation of the US-Iran war. The S&P 500 gained 3.4%, small caps (Russell 2000) gained 3.3%, and the yield on the 10-year Treasury fell 8 basis points to end the week at 4.35%.[1]

- National housing prices rose by 0.9% year-over-year (YoY) in January (latest available) per the S&P CoreLogic National Housing Price Index. This was a smaller increase than December’s 1.1% YoY rate.[1]

- Retail sales came in stronger than expected in February, increasing 0.6% month-over-month (MoM), well ahead of January’s 0.1% MoM decline. Excluding the volatile auto and gas categories, retail sales rose 0.4% MoM, suggestive of stable consumer spending last month.[1]

- The ISM Manufacturing PMI surprised to the upside, increasing to 52.7 in March—any number above 50 denotes expansion—which was a slight increase from February’s 52.4 reading. However, there was a large jump in the prices-paid component to 78.3—the highest level since Jun-2022—which suggests input price inflation remains a problem for the US manufacturing sector.[1]

- Job openings declined in February (latest available) to 6.88 million, a decline of nearly 5% from January’s 7.24 million postings. The number of quits fell to 2.97 million, the lowest level since August 2020. The quit rate is seen as a measure of workers’ confidence in the labor market.[1]

- Initial unemployment claims, however, remain very low, falling to 202k new claims last week—a decrease of 9k from the week prior and 15k fewer claims than the same week last year.[1]

- The March employment numbers were ahead of expectations (+65k), registering 178k new jobs, while both the unemployment rate and labor force participation rate fell 0.1 percentage-points to 4.3% and 61.9%, respectively.[1]

EXPECTATIONS

- The Senate passed last week two funding bills for the Department of Homeland Security—which includes airport TSA agents along with Immigration Customs & Enforcement officers—along party-lines lines that should end the shutdown of the final portion of the government that was without appropriated funds. Security lines across the country should improve as a result.[1]

- Fed Chairman Powell gave a speech last week and he reiterated the Fed’s bias towards a wait-and-see approach to Fed’s next policy move given the current state of uncertainty largely stemming from the rise in energy prices and their impact on consumer prices and economic activity. The Fed Fund Futures market, at this point, has priced in no additional Fed action on rates until mid-2027.[1]

ONE MORE THOUGHT: The US-Iran War the Beginning of the End?[1]

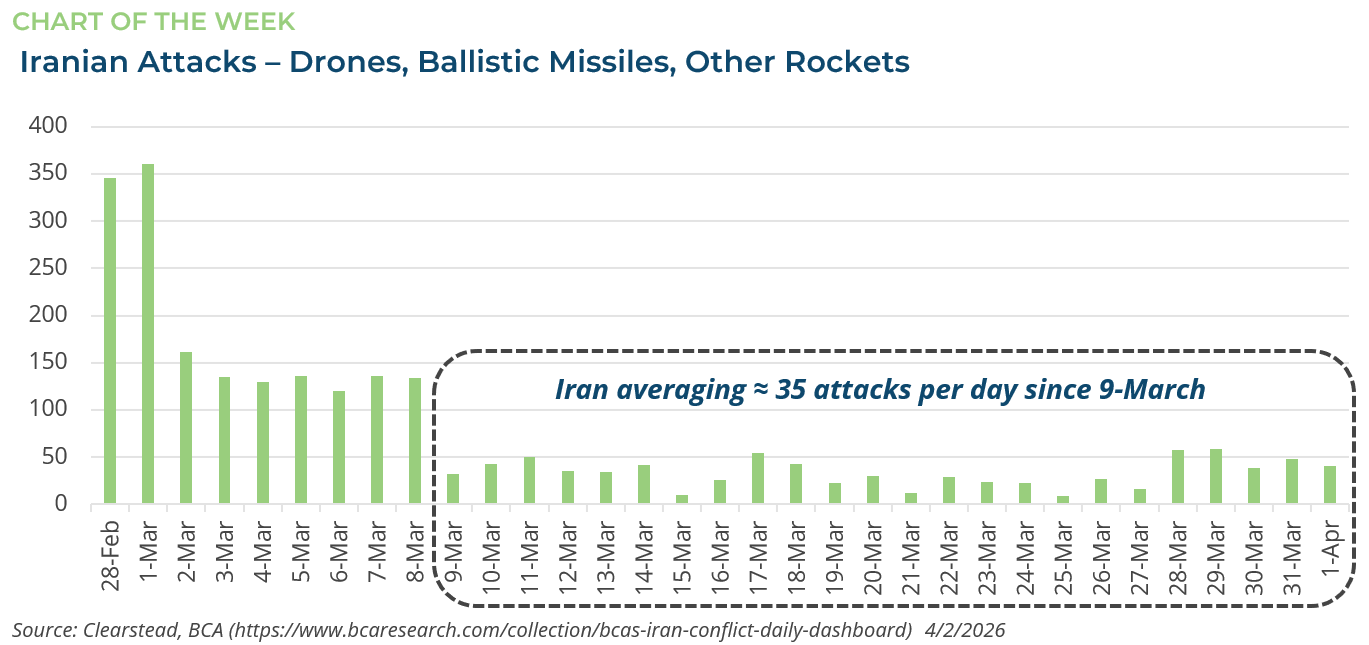

Since the US-Israel launched an attack on Iran in the final days of February, the war has dominated financial markets. Iran’s subsequent closure of the Strait of Hormuz has choked off about 20% of the world’s oil and natural gas supplies. In addition, many oil and gas byproducts have seen supply disruption—urea, helium, sulfur, and Middle Eastern aluminum, amongst others—and the price of these products has increased substantially. For instance, the price of Brent crude increased from about $70 per barrel in late February to nearly $110 per barrel last week. As a result, risk assets have been correlated with daily, war-related headlines. On days that saw the intensification of fighting, energy prices moved higher, while equities moved lower and vice versa. On balance, in the weeks after the war began, investor sentiment deteriorated, and global equities declined. The VIX—the so-called fear gauge—spiked in March and remains elevated. Given that much of Asia and Europe’s oil and gas supply is imported, many countries are facing the prospect of slower growth as consumers and businesses in these regions adjust to higher prices. Some countries might even see a mild recession in 2026—and this risk grows the longer the war continues and the strait remains closed. In the US, households and businesses are facing gasoline at around $4 per gallon, which may weigh on economic activity. This presents investors with a bi-modal outcome over the near-term. Should the war move towards a path of de-escalation, a ceasefire, and/or the re-opening of the Strait of Hormuz, equity markets will likely trade higher. However, if the war were to escalate or be prolonged with little prospect for the Strait to reopen, equity markets would almost certainly trade lower with most major indexes facing another downdraft. President Trump recently addressed the nation, indicating that the war could end in the coming weeks. However, the President did not provide a clear timeline for de-escalation. In times of war, events are fluid, and the likelihood of the two scenarios (escalation or de-escalation) is equally probable. In this market environment, it is easy to get whipsawed by events. Our approach is to ensure that asset allocation is reflective of goals and objectives while using market volatility as an opportunity to rebalance back to long-term targets.

[1] Bloomberg LP, 4/3/2026

Information provided in this article is general in nature, is provided for informational purposes only, and should not be construed as investment advice. These materials do not constitute an offer or recommendation to buy or sell securities. The views expressed by the author are based upon the data available at the time the article was written. Any such views are subject to change at any time based on market or other conditions. Clearstead disclaims any liability for any direct or incidental loss incurred by applying any of the information in this article. All investment decisions must be evaluated as to whether it is consistent with your investment objectives, risk tolerance, and financial situation. You should consult with an investment professional before making any investment decision. Performance data shown represents past performance. Past performance is not an indicator of future results. Current performance data may be lower or higher than the performance data presented. Performance data is represented by indices, which cannot be invested in directly.

Related or Tagged New Posts

market perspectives

April 8th 2026

Quarterly Market Insights | 1Q26 Quarterly

market perspectives

March 30th 2026

Research Corner | 3/30/2026

market perspectives

March 23rd 2026

Research Corner | 3/23/2026

market perspectives

March 16th 2026

Research Corner | 3/16/2026

market perspectives

March 9th 2026

Research Corner | 3/9/2026

market perspectives

March 2nd 2026

Impact of Escalating Conflict in Iran

market perspectives

March 2nd 2026

Research Corner | 3/2/2026

market perspectives

February 23rd 2026

Research Corner | 2/23/2026

market perspectives

February 16th 2026

Research Corner | 2/16/2026

market perspectives

February 12th 2026

Market Update | US Dollar Debasement

market perspectives

February 9th 2026

Research Corner | 2/9/2026

market perspectives

February 2nd 2026

Research Corner | 2/2/2026