OBSERVATIONS

- Markets traded higher last week, with the S&P 500 gaining 0.3% and small caps (Russell 2000) gaining 3.3%, while the yield on the 10-year Treasury fell 6 basis points to end the week at 4.26%.[1]

- The national home builder survey fell 1 point in August to 32—any number below 50 denotes a majority of home builders are pessimistic about the current and near-term outlook for housing—the survey has had a reading below 50 in every month since May-2024.[1]

- Housing starts jumped in July to 1.428 million (annualized rate), which was 5.2% month-over-month (MoM) increase over new housing starts in June, led by a multi-family units which increased 11.6% MoM in July. New home building permits, however, fell by 2.8% MoM in July to 1.393 million (annualized rate). Compared to last year, new home building permits are 5.7% lower than in Jul-2024.[1]

- Existing home sales also increased in July gaining 2.0% MoM to 4.01 million (annualized rate).[1]

- The Architectural Billing index—a leading indicator of non-residential construction—declined in July to 46.2, any number below 50 indicates a majority of firms are seeing declines in billings. The index has been below 50 for 31 of the past 34 months with the weakest readings coming from the Midwest region.[2]

- Initial unemployment claims increased last week by 11k from the week prior to 235k new claims. Overall, unemployment claims remain low and on-par with claims from the same week last year.[1]

EXPECTATIONS

- The minutes of the most recent Fed meeting—held before the July jobs report—showed that while Fed officials worried about the weakening of the US labor market, the majority of Fed officials indicated that the chance of higher inflation due to the new tariff policies enacted was “the greater of these two risks.”[1]

- Fed Chairman Jerome Powell, however, seemed to signal at last week’s Jackson Hole speech that the Fed was now more concerned about the recent labor market weakening and a forth coming rate cut might be warranted.[1]

ONE MORE THOUGHT: A calm August market may set up a more volatile September[1]

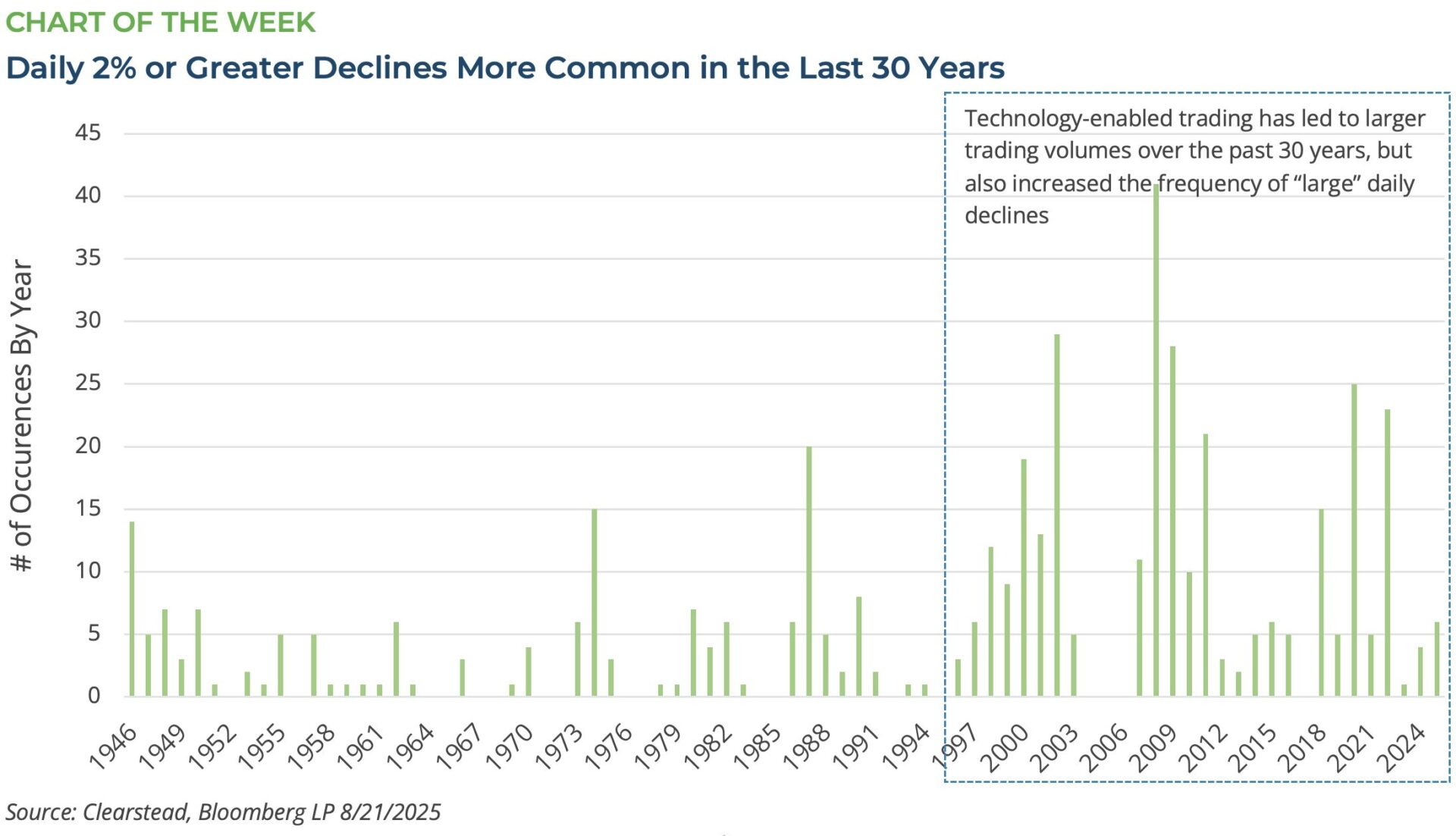

So far, equity market trading in August has remained calm. Clearstead has noted in recent weeks (RC 18-Aug, RC 11-Aug, RC 4-Aug) numerous signs of investor complacency that have emerged despite the uncertain macroeconomic environment. While H1-2025 corporate earnings have been strong and the US economy, thus far, has shown resilience, the full impact of the US’s new tariff policy is still not known. Nonetheless, investors in US equity markets seem to have fully discounted the likelihood of any worst-case scenario vis-à-vis tariffs. Furthermore, at present they seem to be gripped with the notion that interest rate cuts are imminent, tariff impacts are largely negligible, and US consumers can keep spending. All of these assumptions are likely to be tested in the coming weeks. The S&P 500 has hit three separate record highs so far in August. What is more, volatility, which has been muted in August as trading volume typically hits its annual lows, is likely to re-emerge as traders return to their desks in September. In fact, the S&P 500 has not seen a daily decline of 2% or more since late April. Over the past thirty years, a daily decline of 2% or more occurs between 10-11 times per year—see Chart of the Week. So far in 2025, we have had six such declines—five of which occurred in the first three weeks of April—which suggests that additional volatility may be in the cards in the final months of the year. Prior to the mid-1990s and the rise of more technology-enabled, quantitatively driven trading volume, a daily decline of 2% of more was relatively rare. In the 50 years between 1946 and 1995, a daily decline of 2% or more occurred only about three times per year and there were only three years (1946, 1974, and 1987) that saw more than 10 occurrences of declines of this magnitude. In contrast, 12 of the past 30 years have seen such declines occurring 10 times or more during the year. Now, there still have been years in the recent past that have exhibited few occurrences of these types of declines, such as 2004, 2005, 2006, 2017, and 2023, but in each of these instances the global economy, as well as the US economy, were experiencing strong growth. However, in terms of this year, while the US economy is showing stable (albeit sub-trend) growth, much of the rest of the developed world—Europe, Canada, UK, and Japan—are seeing weak economic growth and each could experience a mild recession in the quarters ahead. All this suggests that volatility is likely to return to equity markets—thus a rebalancing back to equity targets is warranted, and patient, long-term investors should not lose sight of their ability to deploy money into advantageous entry points.

[1] Bloomberg LP, 8/22/2025

[2] https://live-aia-web.pantheonsite.io/resource-center/abi-july-2025-business-architecture-firms-remains-soft

Information provided in this article is general in nature, is provided for informational purposes only, and should not be construed as investment advice. These materials do not constitute an offer or recommendation to buy or sell securities. The views expressed by the author are based upon the data available at the time the article was written. Any such views are subject to change at any time based on market or other conditions. Clearstead disclaims any liability for any direct or incidental loss incurred by applying any of the information in this article. All investment decisions must be evaluated as to whether it is consistent with your investment objectives, risk tolerance, and financial situation. You should consult with an investment professional before making any investment decision. Performance data shown represents past performance. Past performance is not an indicator of future results. Current performance data may be lower or higher than the performance data presented. Performance data is represented by indices, which cannot be invested in directly.

Related or Tagged New Posts

market perspectives

March 16th 2026

Research Corner | 3/16/2026

market perspectives

March 9th 2026

Research Corner | 3/9/2026

market perspectives

March 2nd 2026

Impact of Escalating Conflict in Iran

market perspectives

March 2nd 2026

Research Corner | 3/2/2026

market perspectives

February 23rd 2026

Research Corner | 2/23/2026

market perspectives

February 16th 2026

Research Corner | 2/16/2026

market perspectives

February 12th 2026

Market Update | US Dollar Debasement

market perspectives

February 9th 2026

Research Corner | 2/9/2026

market perspectives

February 2nd 2026

Research Corner | 2/2/2026

market perspectives

January 26th 2026

Research Corner | 1/26/2026

market perspectives

January 20th 2026

Research Corner | 1/20/2026

market perspectives

January 12th 2026

Quarterly Market Insights | 4Q25