OBSERVATIONS

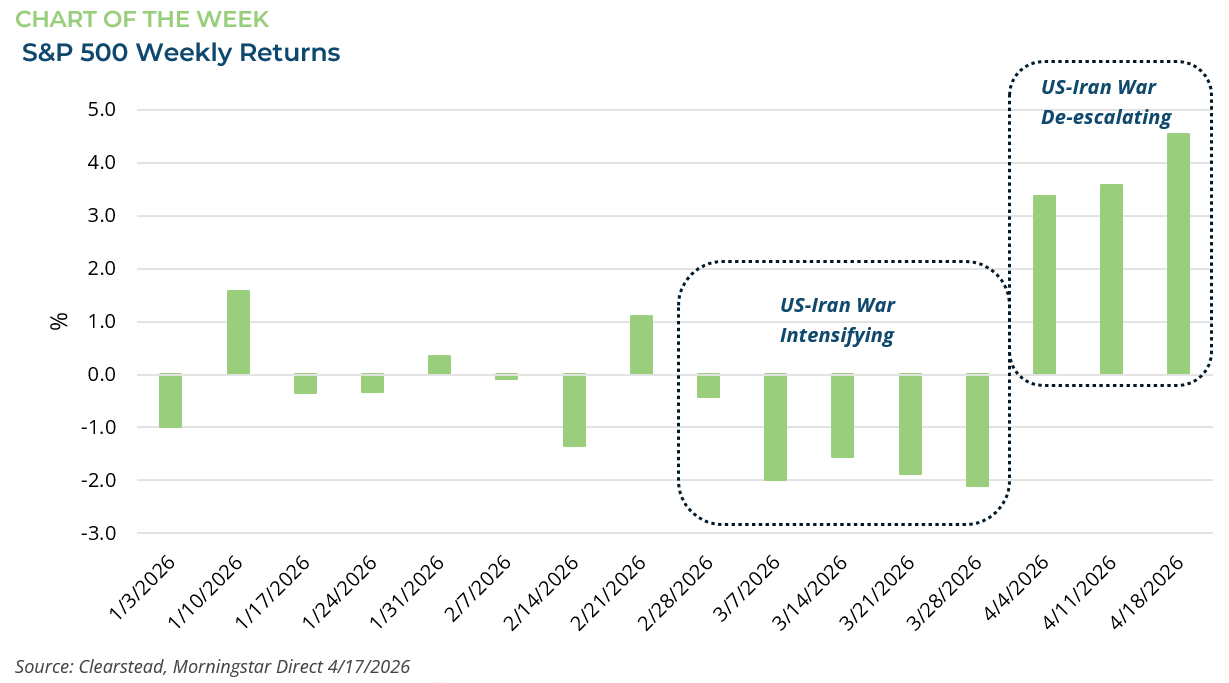

- Markets traded higher amid ongoing US-Iran talks, the S&P gained 4.6% and small caps (Russell 2000) gained 5.6%, while the yield on the 10-year Treasury fell 7 basis point to end the week at 4.25%.[1]

- Small business optimism fell to 95.8, below its 52-year average of 98. Declines were seen across most subcomponents, with the largest drops coming in “small business current earnings trends” and “expectations for the economy to improve and better business conditions to develop.”[1]

- Existing home sales fell by 3.6% month-over-month (MoM) in March to 3.98 million (annualized), with monthly declines in all regions. Existing home sales were down by 1% year-over-year (YoY).[1]

- The National Home Buying Index fell 4 points to 34—a reading <50 suggests that a majority of home builders feel pessimistic about the current and near-term outlook—with declines in all sub-components including current sales conditions, expectations for future sales, and current foot traffic in model homes.[1]

- Prices at the wholesale level increased less than expected in March but still showed inflationary pressures, with the headline PPI showing the wholesale prices increased to 4.0% YoY, up from 3.4% YoY in February. Excluding the volatile food and energy categories, core-PPI held steady at 3.8% YoY.[1]

- Initial unemployment claims remain very low registering only 207k new claims last week, which was an 11k decline from the week prior and about 7k fewer than the same week last year.[1]

- Industrial production declined by 0.1% MoM in March with declines across all three sub-sectors—manufacturing (-0.1% MoM), mining (-1.2% MoM) and utilities (-2.3% MoM). Industrial capacity utilization slipped by 40 basis points to 75.7% which is 3.7 percentage points below its long-run average.[1]

EXPECTATIONS

- The Fed’s Beige Book—a qualitative assessment of the US economy by Fed districts—suggests the US economy remains stable. The April reports indicate that economic activity increased modestly in eight of the twelve districts. Two districts reported little change, and two districts reported modest declines.[2]

- Q1 earnings are off to a good start. Only about 10% of the S&P 500 have reported Q1 earnings, but so far 88% of companies are reporting a positive earnings surprise, which is better than the 5-year (78%) and the 10-year (76%) average. Overall, Q1 earnings are on track to grow by 13.2% YoY.[3]

ONE MORE THOUGHT: S&P Sets New Record High and Closes Above 7,000[1]

After five straight weeks of declines in the S&P 500, the move between the US and Iran to begin negotiations towards a ceasefire prompted a strong shift in sentiment. At the end of March, the S&P 500 had declined over 9% from its all-time high which was set in late January. However, since the US-Iran ceasefire talks began, markets began to trade higher and for three consecutive weeks the S&P 500 made strong gains, which culminated in the setting of three new record highs last week. It should be no surprise that given these strong gains, various measures of investor sentiment have moved decidedly from negative to positive. For instance, the VIX Index—the so called “fear gauge”—spiked above 35 during the height of tensions in late March and remained elevated into early April. In recent weeks it has receded sharply and finished last week at 17.5, which is below its long-run average (19.0). During the sell-off in March, quantitative investors aggressively sold down their global equity exposure. Once ceasefire talks commenced, these same investors raced to get back into global equities. Similarly, other measures of investor sentiment such as the put-call ratio and the bull-bear survey all suggested that a risk-on mentality has re-emerged within US equities. Equally, it was not just the S&P 500 that is flourishing. The NASDAQ 100 Index as well as the Russell 2000 Index (small caps) also hit record highs last Friday. Clearstead had judged that markets were poised for a bimodal outcome as a result of the US-Iran war. An escalation of the conflict and a longer closure of the Strait of Hormuz would take equities lower, while a de-escalation and path towards a credible ceasefire would take equities higher (and oil prices lower). Thus far, the latter scenario seems to be playing out. While there remain risks that US-Iran talks will not be fruitful, on balance we judge that there are enough incentives on both sides to keep talking rather than resume the conflict. Even in the event the ceasefire holds, the Strait of Hormuz fully re-opens, and energy markets normalize, some semi-permanent damage will have been done to global growth this year. However, as the geopolitical shock fades, investors will once again likely refocus their attention on corporate earnings, which still look promising—particularly within the US.

[1] Bloomberg LP, 4/17/2026

[2] www.federalreserve.gov/monetarypolicy/files/BeigeBook_20260415.pdf

[3] FactSet Earnings Insight 4/17/2026

Information provided in this article is general in nature, is provided for informational purposes only, and should not be construed as investment advice. These materials do not constitute an offer or recommendation to buy or sell securities. The views expressed by the author are based upon the data available at the time the article was written. Any such views are subject to change at any time based on market or other conditions. Clearstead disclaims any liability for any direct or incidental loss incurred by applying any of the information in this article. All investment decisions must be evaluated as to whether it is consistent with your investment objectives, risk tolerance, and financial situation. You should consult with an investment professional before making any investment decision. Performance data shown represents past performance. Past performance is not an indicator of future results. Current performance data may be lower or higher than the performance data presented. Performance data is represented by indices, which cannot be invested in directly.

Related or Tagged New Posts

market perspectives

August 3rd 2026

Research Corner | 8/3/2026

market perspectives

July 27th 2026

Research Corner | 7/27/2026

market perspectives

July 20th 2026

Research Corner | 7/20/2026

market perspectives

July 13th 2026

Research Corner | 7/13/2026

market perspectives

July 8th 2026

Quarterly Market Insights | 2Q26

market perspectives

July 6th 2026

Research Corner | 7/6/2026

market perspectives

June 29th 2026

Research Corner | 6/29/2026

market perspectives

June 22nd 2026

Research Corner | 6/22/2026

market perspectives

June 15th 2026

Research Corner 6/15/2026

market perspectives

June 8th 2026

Research Corner 6/8/2026

market perspectives

June 1st 2026

Research Corner | 6/1/2026

market perspectives

May 26th 2026

Research Corner | 5/26/2026