OBSERVATIONS

- Markets traded flat last week with the S&P 500 gaining 0.6% and small caps (Russell 2000) gaining 0.4%, while the yield on the 10-Year Treasury gained 5 basis points to end the week at 4.30%.[1]

- Retail sales were stronger than expected in March, with the headline retail sales figure registering 1.7% month-over-month (MoM) growth. Compared to March 2025, retail sales were up 4.0% year-over-year (YoY). Excluding the volatile auto and gas categories, retail sales increased 0.6% MoM—exceeding expectations—and 4.2% YoY.[1]

- The Architecture Billing Index increased slightly in March to 49.8—a score above 50 indicates a majority of architectural firms saw an increase in billing activity. The index, which is a 9-to-12-month leading indicator of non-residential construction activity, has been below 50 for all but one month since October-2022.[1]

- Unemployment claims remain low but ticked up 6k from the week prior to reach 214k new claims. However, there were 5k fewer claims last week than in the same week in 2025. Overall, through the first 16 weeks of 2026, there have been 3.6% fewer unemployment claims than in the first 16 weeks of 2025.[1]

EXPECTATIONS

- Fed Chairman-elect Kevin Warsh testified before the Senate Banking Committee last week and made his case that he would champion Fed independence as it pertains to setting monetary policy. A formal vote on his nomination may be coming soon as the Senate committee may advance his nomination for a full Senate vote in the coming weeks because the Department of Justice probe into current Fed Chairman Powell over the cost overruns of the new Fed building seems to be resolved.[1]

- The Fed will meet this week to review monetary policy. In the lead-up to the meeting, most Fed speakers have echoed Powell’s assessment that the current policy rates (3.5% to 3.75%) are appropriate, and that the Fed is in a good position to wait-and-see how the economy evolves before altering policy.[1]

- So far about 28% of the S&P 500 have reported Q1 earnings, and 84% of companies are reporting a positive earnings surprise, which is better than the 5-year (78%) and the 10-year (76%) average. Overall, Q1 earnings are on track to grow by 15.1% YoY.[2]

- Notably in terms of CY2026 earnings, the Technology sector is poised to account for approximately 60% of the S&P 500 total earnings growth this year.[2]

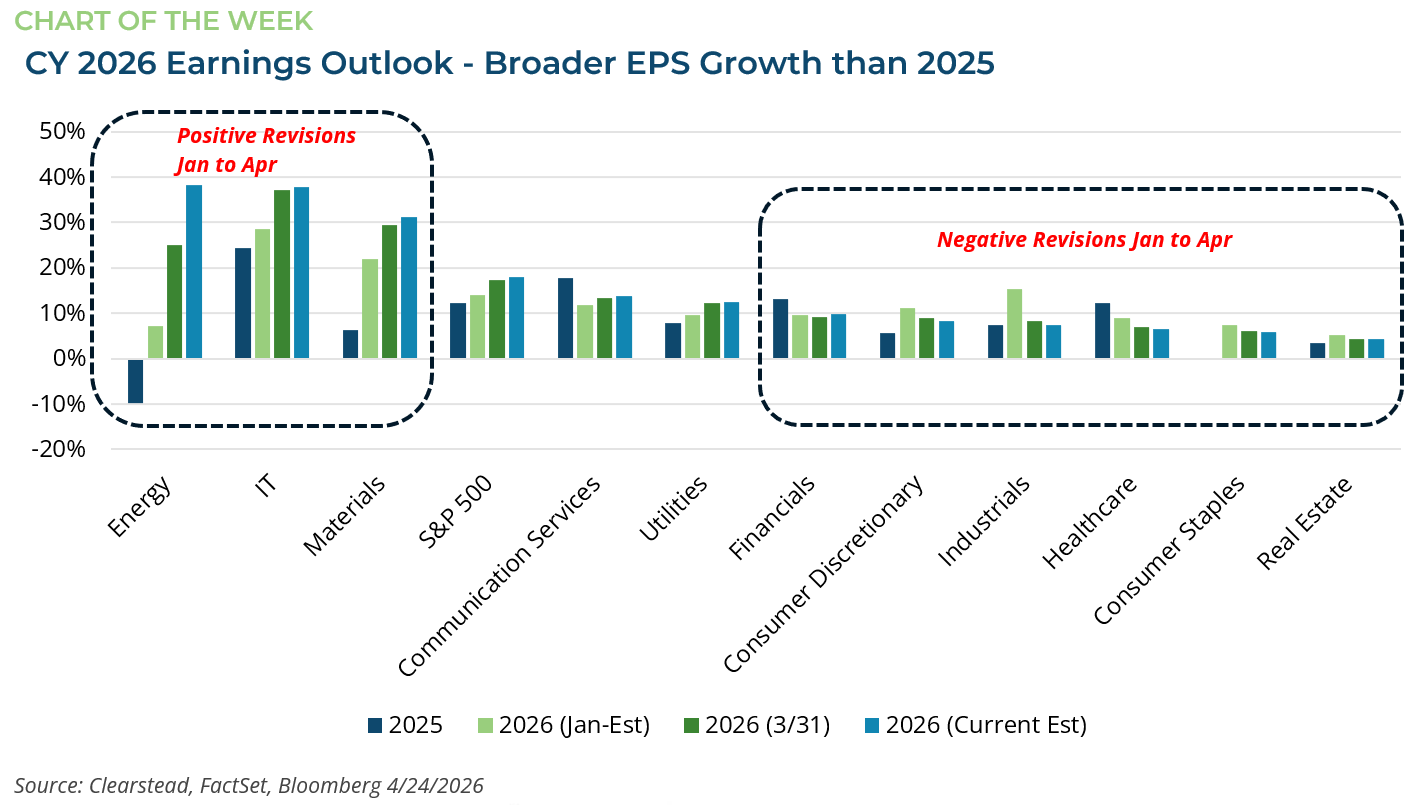

ONE MORE THOUGHT: Earnings Revisions Have Been Positive, But Narrow[1,2]

The US-Iran War is still unresolved, and the vital Strait of Hormuz remains largely blocked. Even so, earnings estimates for US companies continue to trend higher. As noted earlier, the Q1 earnings season is off to a strong start, with a key theme being that the US consumers are still spending, and the economy remains stable. Higher energy prices, such as oil and gas, typically hurt earnings because they raise costs and squeeze profit margins. Despite this, analysts have been raising their earnings forecasts for 2026. While headlines suggest that earnings revisions are strong overall, this obfuscates an important detail: only a small number of sectors and companies are driving the gains. Of the eleven equity sectors in the S&P 500, only three – Energy, Materials, and Technology – have seen material positive revisions this year. Six sectors have had their earnings estimates revised down since the year began. Even within Energy and Technology, most of the gains come from just a few companies. In Technology, nearly all the positive revisions come from just three companies—Micron (+93%), Broadcom (+44), and Sandisk (+24%). Similarly, in the Energy sector, six companies—Occidental (+251%), Valero (+79%), ConocoPhillips (+76%), Chevron (+67%), EOG Resources (+51%), and ExxonMobil (44%)—account for nearly all the positive revisions. Looking more closely at Q1 2026 earnings, the “Mag7” stocks—Alphabet, Amazon, Apple, Meta, Microsoft, NVDIA, and Tesla—are expected to grow earnings by about 22%. The S&P 493 (the remainder of the index) is expected to increase earnings by about 10%. If NVIDIA were excluded from the Mag7, the remaining six companies would only be growing earnings by about 6%. Even though earnings growth is concentrated in a few sectors, most companies are expected to have better earnings in 2026 than in 2025. While headlines focus on the S&P 500 reaching record highs in recent weeks, they often overlook that fewer stocks are driving those gains. This narrowing market strength could lead to a more uneven path for equities, as much of this year’s good news may already be reflected in current prices.

[1] Bloomberg LP, 4/24/2026

[2] FactSet Earnings Insight 4/24/2026

Information provided in this article is general in nature, is provided for informational purposes only, and should not be construed as investment advice. These materials do not constitute an offer or recommendation to buy or sell securities. The views expressed by the author are based upon the data available at the time the article was written. Any such views are subject to change at any time based on market or other conditions. Clearstead disclaims any liability for any direct or incidental loss incurred by applying any of the information in this article. All investment decisions must be evaluated as to whether it is consistent with your investment objectives, risk tolerance, and financial situation. You should consult with an investment professional before making any investment decision. Performance data shown represents past performance. Past performance is not an indicator of future results. Current performance data may be lower or higher than the performance data presented. Performance data is represented by indices, which cannot be invested in directly.

Related or Tagged New Posts

market perspectives

July 20th 2026

Research Corner | 7/20/2026

market perspectives

July 13th 2026

Research Corner | 7/13/2026

market perspectives

July 8th 2026

Quarterly Market Insights | 2Q26

market perspectives

July 6th 2026

Research Corner | 7/6/2026

market perspectives

June 29th 2026

Research Corner | 6/29/2026

market perspectives

June 22nd 2026

Research Corner | 6/22/2026

market perspectives

June 15th 2026

Research Corner 6/15/2026

market perspectives

June 8th 2026

Research Corner 6/8/2026

market perspectives

June 1st 2026

Research Corner | 6/1/2026

market perspectives

May 26th 2026

Research Corner | 5/26/2026

market perspectives

May 18th 2026

Research Corner | 5/18/2026

market perspectives

May 11th 2026

Research Corner | 5/11/2026