OBSERVATIONS

- Markets were mixed last week with the S&P 500 gaining 0.2%, while small caps (Russell 2000) declined 2.3%. The S&P 500 closed at a record above 7,500 last Thursday. The yield on the 10-year Treasury rose23 basis points to end the week at 4.59%.[1]

- Small business optimism was largely unchanged in April, increasing 0.1 points to 95.9, but remained below its 52-year average of 98. Notably, the share of business owners reporting higher sales is now at a 12-month low.[1]

- Existing home sales increased 0.2% month-over-month (MoM) to an annualized rate of 4.02 million units, below expectations of 4.05 million. On a year-over-year (YoY) basis, existing home sales were unchanged.[1]

- Headline inflation increased to 3.8% YoY in April, exceeding expectations of 3.7% and March’s 3.3% inflation rate. Core CPI, which excludes food and energy, increased to 2.8% YoY in April from 2.6% YoY in March.[1]

- Wholesale prices also came in higher than expected. Headline PPI rose to 6.0% YoY in April, well above 4.3% YoY in March. Core PPI, excluding food and energy, increased from 4.0% YoY in March to 5.2% YoY in April.[1]

- Retail sales in April were largely in line with expectations, with topline sales rising 0.5% MoM. Retail sales excluding autos and gas also increased by 0.5% MoM, slightly ahead of expectations.[1]

- Initial unemployment claims increased to 211k, a 12k increase from the prior week. Overall claims remain low and are 13k fewer than the same week last year.[1]

- April industrial production rose 1.4% YoY and 0.7% MoM, beating Street consensus of 0.3% MoM growth. Among sub-components, energy, consumer products, and commercial products rose by 2.1%, 4.2%, and 4.1% YoY, respectively.[1]

EXPECTATIONS

- The Senate confirmed Kevin Warsh to the Federal Reserve Board of Governors and endorsed him as the next Fed Chair last week. Warsh will replace Jerome Powell, whose term as Chair ended last Friday. Powell may remain a voting Board Governor until 2028, and he has indicated he will forego retirement to remain at the Fed until the legal investigations into alleged Fed corruption are resolved.[1]

- Q2 earnings season is nearly complete, with approximately 90% of companies having reported results. NVIDIA, Broadcom, and Salesforce are the only remaining companies likely to have a material impact on overall results. Of the 443 companies that reported, 84% delivered a positive surprise, above the 5-year average (78%) and the 10-year average (76%). In aggregate, the reporting companies beat Street estimates by 17.8%! Q1 earnings are currently on track to grow 27.1% YoY.[2]

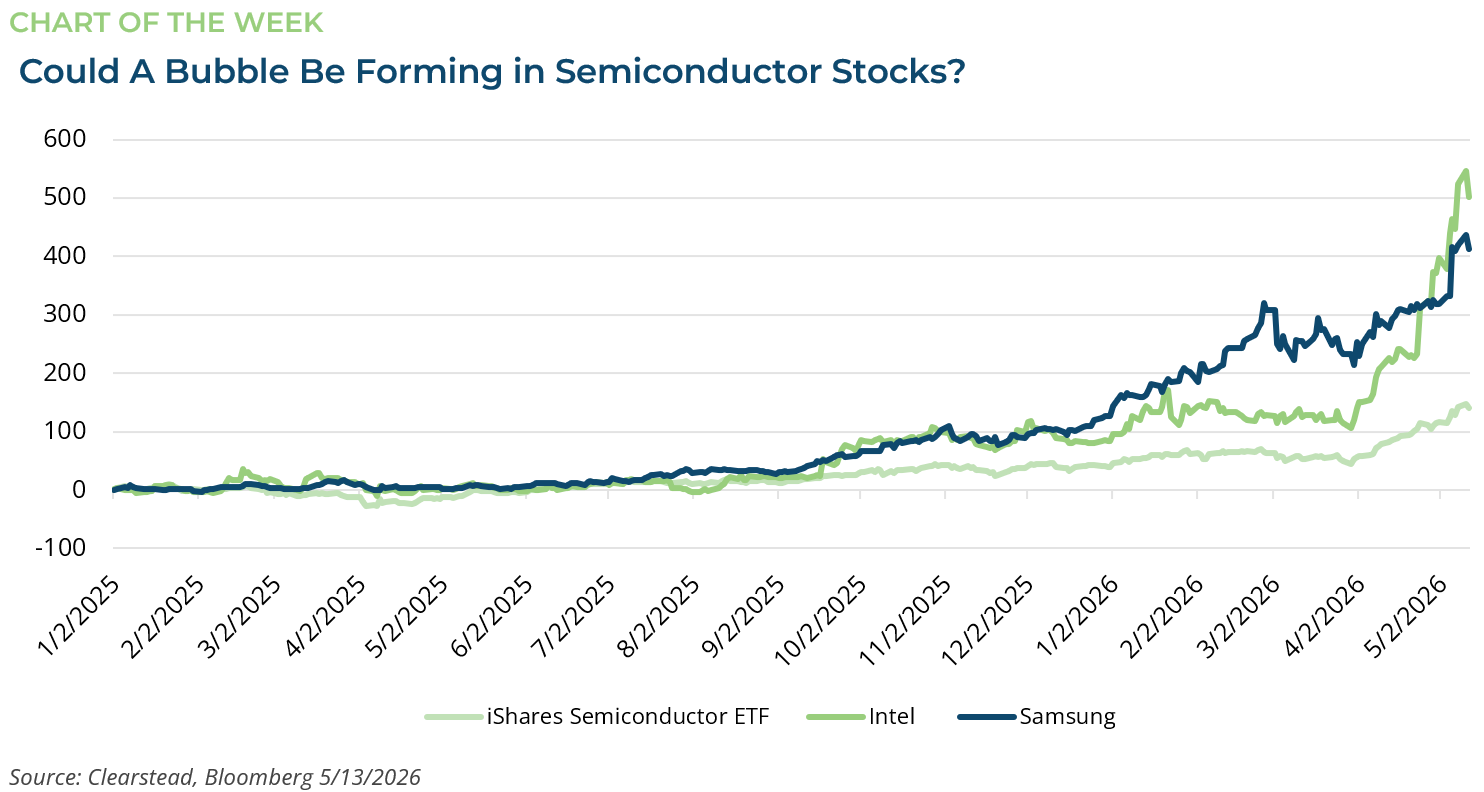

ONE MORE THOUGHT: Semiconductors and AI Lead an Increasingly Narrow Market [1,3]

U.S. equity markets continued to move higher last week, driven mainly by large-cap growth stocks. The S&P 500 reached three new record highs, bringing its year-to-date total to 18, while the Nasdaq also set fresh highs. Notably, 12 of the S&P 500’s 18 records have come since mid-April—roughly one new high every other trading day. At the same time, market leadership has become increasingly concentrated in a small group of AI-related stocks. For example, Intel (INTC) rose from about $44 at the end of March to $120 by the end of last week, nearly tripling in just over six weeks. The SOXX semiconductor ETF also gained more than 1.5x over that period. Samsung, whose memory chips are critical to AI data center infrastructure, has nearly doubled as well, supported by reports that its memory chip capacity is sold out through the end of 2027. These moves suggest speculative activity may be driving momentum in AI-related stocks. Bloomberg has noted that more than 60% of daily trading volume comes from short-term participants, including high-frequency trading firms and retail investors. That backdrop can fuel momentum-driven price action and temporarily disconnect valuations from fundamentals as investors display herd behavior. As noted previously, spending on AI infrastructure remains significant and is supporting both real economic activity and incremental cash flow for companies building out the ecosystem. At the same time, these outsized returns have drawn substantial investor interest. In April, semiconductor- and memory-chip-focused South Korean ETFs attracted $2.3 billion in inflows, while U.S. technology sector ETFs drew $12 billion. The AI story remains compelling, but the speed and magnitude of recent gains suggest that volatility may increase in the weeks and months ahead. Sentiment-driven market moves can reverse quickly.

[1] Bloomberg LP, 5/15/2026

[2] FactSet Earnings Insight 5/15/2026

[3] State Street – ETF Investment Management Chart Pack May-2026

Information provided in this article is general in nature, is provided for informational purposes only, and should not be construed as investment advice. These materials do not constitute an offer or recommendation to buy or sell securities. The views expressed by the author are based upon the data available at the time the article was written. Any such views are subject to change at any time based on market or other conditions. Clearstead disclaims any liability for any direct or incidental loss incurred by applying any of the information in this article. All investment decisions must be evaluated as to whether it is consistent with your investment objectives, risk tolerance, and financial situation. You should consult with an investment professional before making any investment decision. Performance data shown represents past performance. Past performance is not an indicator of future results. Current performance data may be lower or higher than the performance data presented. Performance data is represented by indices, which cannot be invested in directly.

Related or Tagged New Posts

market perspectives

July 20th 2026

Research Corner | 7/20/2026

market perspectives

July 13th 2026

Research Corner | 7/13/2026

market perspectives

July 8th 2026

Quarterly Market Insights | 2Q26

market perspectives

July 6th 2026

Research Corner | 7/6/2026

market perspectives

June 29th 2026

Research Corner | 6/29/2026

market perspectives

June 22nd 2026

Research Corner | 6/22/2026

market perspectives

June 15th 2026

Research Corner 6/15/2026

market perspectives

June 8th 2026

Research Corner 6/8/2026

market perspectives

June 1st 2026

Research Corner | 6/1/2026

market perspectives

May 26th 2026

Research Corner | 5/26/2026

market perspectives

May 11th 2026

Research Corner | 5/11/2026

market perspectives

May 4th 2026

Research Corner | 5/4/2026