OBSERVATIONS

- Markets were lower last week, with the S&P 500 losing 2.6% and small caps (Russell 2000) losing 2.9%, while the yield on the 10-year Treasury rose 9 basis points to end the week at 4.53%.[1]

- The ISM Manufacturing PMI rose to 54 in May—any number above 50 denotes expansion—up 1.3 from April’s 52.7 reading and the highest level since May 2022. The prices paid component remains elevated at 82.1, suggesting input price inflation may be a sustained problem.[1]

- The ISM Services PMI beat expectations, registering 54.5 in May, up from 53.6 in April, and the 23rd consecutive month the services PMI has been above 50.[1]

- Nonfarm productivity was revised down by 0.1pp to +2.8% year-over-year (YoY) for Q1-2026, but remained above the 10-year average of 2.0% YoY productivity gains.[1]

- Job openings increased in April (latest available) to 7.618 million openings—well ahead of expectations—and an increase of over 700k postings from March’s figure.[1]

- Initial unemployment claims remain very low, registering 225k claims last week, an increase of 13k from the week prior. However, claims were nearly 20k fewer compared to the same week last year.[1]

- The May jobs report solidly beat expectations (consensus was for 80k) with 172k new jobs created last month and the initial estimate for April’s jobs revised higher from 115k to 179k and the final estimate for March was also revised higher to 214k. Meanwhile the unemployment rate held steady at 4.3% in May and labor force participation was also unchanged in May at 61.8%.[1]

EXPECTATIONS

- The Fed’s May Beige Book—a qualitative assessment of the US economy in each of the twelve Fed districts—continues to show a resilient economy with 10 out of the 12 districts reporting a slight to moderate increase in economic activity, while one district reported a slight decline and one reported no change. Consumer spending remains dispersed across income groups amid affordability pressures, with districts noting increased credit card usage, fewer retail visits, and stronger demand for necessities.[1]

- Canada’s economy entered a mild recession as recent data showed that the Canadian economy contracted by 0.1% in Q1 (annualized rate) after experiencing a 0.2% decline in Q4. Canada’s economy has only one quarter of positive growth in the past four quarters as it is struggling due to less trade with the US (see One More Thought) and less government spending.[1]

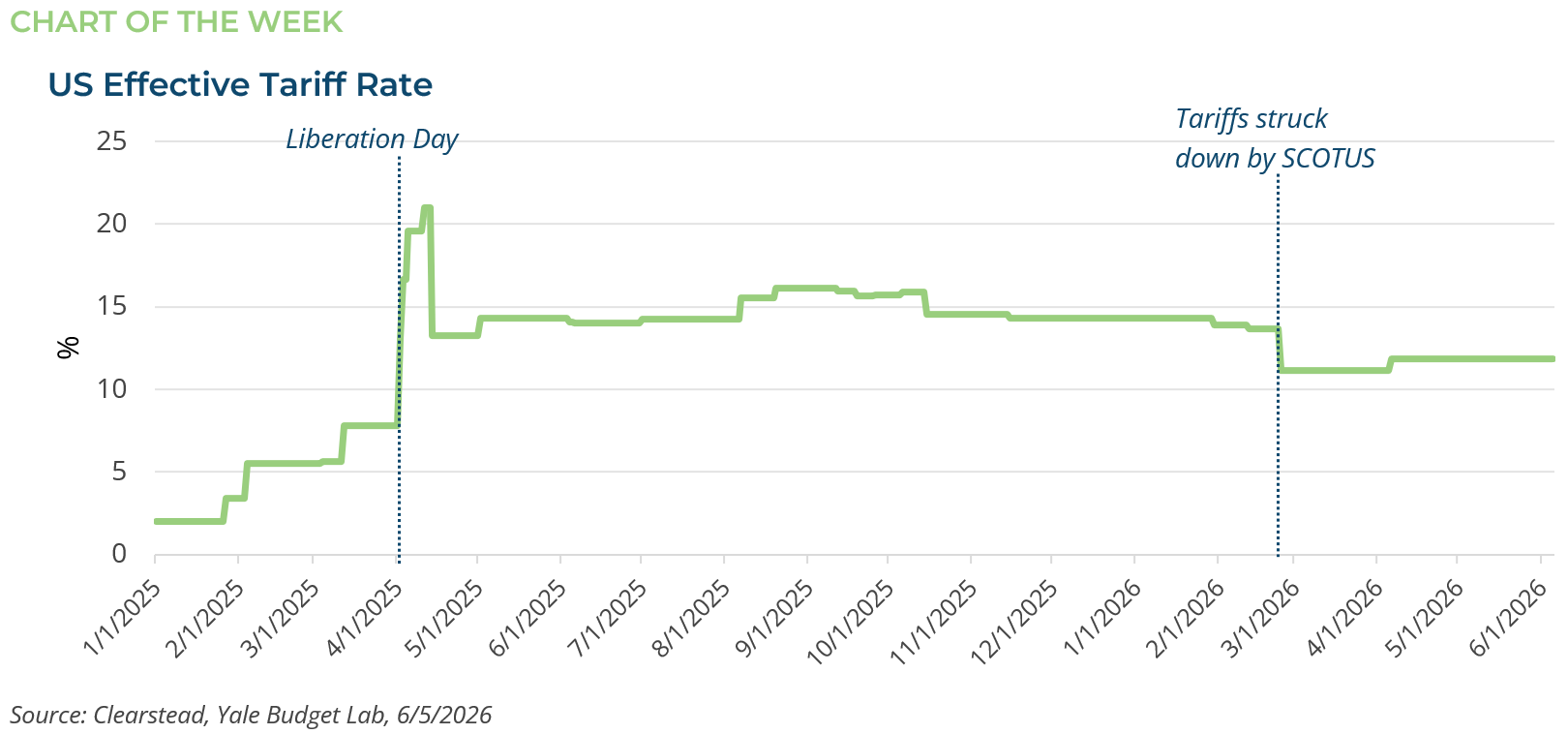

ONE MORE THOUGHT: Trump Administration’s New Tariff Policy[1]

The Trump Administration continues to use tariffs as a central tool for reshaping the US economy. After its original policy was struck down by the Supreme Court as illegal (see RC 2-Mar) in late February, the Administration reimposed a flat 10% tariff under Section 232 of the 1974 Trade Act. Those tariffs can remain in effect for only 150 days—roughly until mid-July—unless Congress reauthorizes them. At the same time, the Administration launched a series of Section 301 investigations into whether individual countries were creating burdens to commerce (trade barriers) or engaging in unfair trade practices under the 1974 Trade Act. Last week, the Office of the US Trade Representative released the results of those investigations, alleging that 60 countries—including many of the US’s largest trading partners—failed to effectively prohibit or enforce bans on goods made with forced labor and therefore could legally be subject to tariffs until compliance improves. Under the proposal, Canada, Mexico, the European Union, the United Kingdom, Taiwan, and 10 smaller countries would face a 10% tariff, while the other 45 countries—including China, India, Brazil, and South Korea—would face a 12.5% tariff. These tariffs would not take effect immediately; instead, they are subject to a 30-day public comment period and a public hearing scheduled for 7-July. As a result, the final scope, timing, and any exemptions could shift over the coming month. Goods and services covered under the US-Mexico-Canada Agreement (USMCA) would remain exempt. However, the US is set to begin its USMCA review on 1-July. The agreement includes a 16-year extension that must be reviewed and confirmed by all three parties. Canada and Mexico have both called for a clean 16-year extension, but the Trump Administration has signaled deep dissatisfaction with the current trade balance between the US and its free-trade partners and appears likely to seek changes to the agreement before approving any extension. So far, bilateral meetings between the US and Canada have made little progress, while talks with Mexico appear to be moving further along. A central issue with Mexico is a loophole that allows Chinese-manufactured goods to be assembled there into final products and then enter the US tariff-free. Canada’s economy has been hit hard by higher trade barriers over the past year as it attempts to reduce its reliance on trade with the US. Among other objectives, the US is seeking to ease Canadian restrictions on agricultural and dairy exports and shift more automotive investment from Canada to the US.

[1] Bloomberg LP, 6/5/2026

Information provided in this article is general in nature, is provided for informational purposes only, and should not be construed as investment advice. These materials do not constitute an offer or recommendation to buy or sell securities. The views expressed by the author are based upon the data available at the time the article was written. Any such views are subject to change at any time based on market or other conditions. Clearstead disclaims any liability for any direct or incidental loss incurred by applying any of the information in this article. All investment decisions must be evaluated as to whether it is consistent with your investment objectives, risk tolerance, and financial situation. You should consult with an investment professional before making any investment decision. Performance data shown represents past performance. Past performance is not an indicator of future results. Current performance data may be lower or higher than the performance data presented. Performance data is represented by indices, which cannot be invested in directly.

Related or Tagged New Posts

market perspectives

August 10th 2026

Research Corner 8/10/2026

market perspectives

August 7th 2026

July Review 2026

market perspectives

August 3rd 2026

Research Corner | 8/3/2026

market perspectives

July 27th 2026

Research Corner | 7/27/2026

market perspectives

July 20th 2026

Research Corner | 7/20/2026

market perspectives

July 13th 2026

Research Corner | 7/13/2026

market perspectives

July 8th 2026

Quarterly Market Insights | 2Q26

market perspectives

July 6th 2026

Research Corner | 7/6/2026

market perspectives

June 29th 2026

Research Corner | 6/29/2026

market perspectives

June 22nd 2026

Research Corner | 6/22/2026

market perspectives

June 15th 2026

Research Corner 6/15/2026

market perspectives

June 1st 2026

Research Corner | 6/1/2026