OBSERVATIONS

- Markets were choppy last week but ultimately traded higher. The S&P 500 gained 0.7% and small caps (Russell 2000) gained 3.9%, while the yield on the 10-year Treasury fell 5 basis points to close at 4.48%.1

- The U.S. trade deficit decreased by $0.7 billion to $55.9 billion in April 2026, as exports rose 2.6% to a record $327.1 billion, driven primarily by capital goods, energy, and industrial supplies.1

- Small business optimism fell 0.6 points to 95.3, as the share of owners citing inflation as their most important business problem climbed for a third straight month. This marked the lowest level since October 2024 and erased almost all the gains seen since President Trump was elected for his second term.1

- Existing home sales rose 3.2% month-over-month (MoM) to an annualized rate of 4.17 million. This was the second consecutive monthly gain in existing home sales and the strongest sales figure so far this year.1

- Headline CPI inflation increased to 4.2% year-over-year (YoY) in May, matching expectations but remaining well above April’s 3.8% YoY rate. Energy prices rose 3.9% MoM in May, driving more than half of the increase in the headline inflation figure. Core CPI, which excludes food and energy, increased to 2.9% YoY in May from April’s 2.8% YoY figure.1

- Prices at the wholesale level continued to surge, with the headline PPI index increasing to 6.5% YoY in May, above April’s 5.7% YoY rate. Core PPI, which excludes food and energy, rose 4.9% YoY, unchanged from April’s revised figure.1

- Initial unemployment claims remain low despite increasing by 5k last week to 229k. However, claims were still 15,000 lower than in the same week in 2025.1

- The University of Michigan Consumer Sentiment Index increased in June to 48.9, up over 4 points from May’s 44.8 figure—the lowest reading in the survey’s history—as a broad swath of respondents noted relief as gasoline prices eased in recent weeks.1

EXPECTATIONS

SpaceX went public last week at $135 per share. Approximately 4% of the company’s shares were offered in a heavily over-subscribed IPO that raised about $75 billion—implying a $1.77 trillion market cap for the firm—and marking the largest IPO in history. Trading was choppy on its first day, but the stock opened at $150 a share, traded higher and ultimately closed last Friday at $161 (up nearly 20%)—FTSE-Russell, NASDAQ, and CRSP will add SpaceX to their indices in the coming weeks, while the S&P 500 will consider inclusion after 12 months.1

ONE MORE THOUGHT:

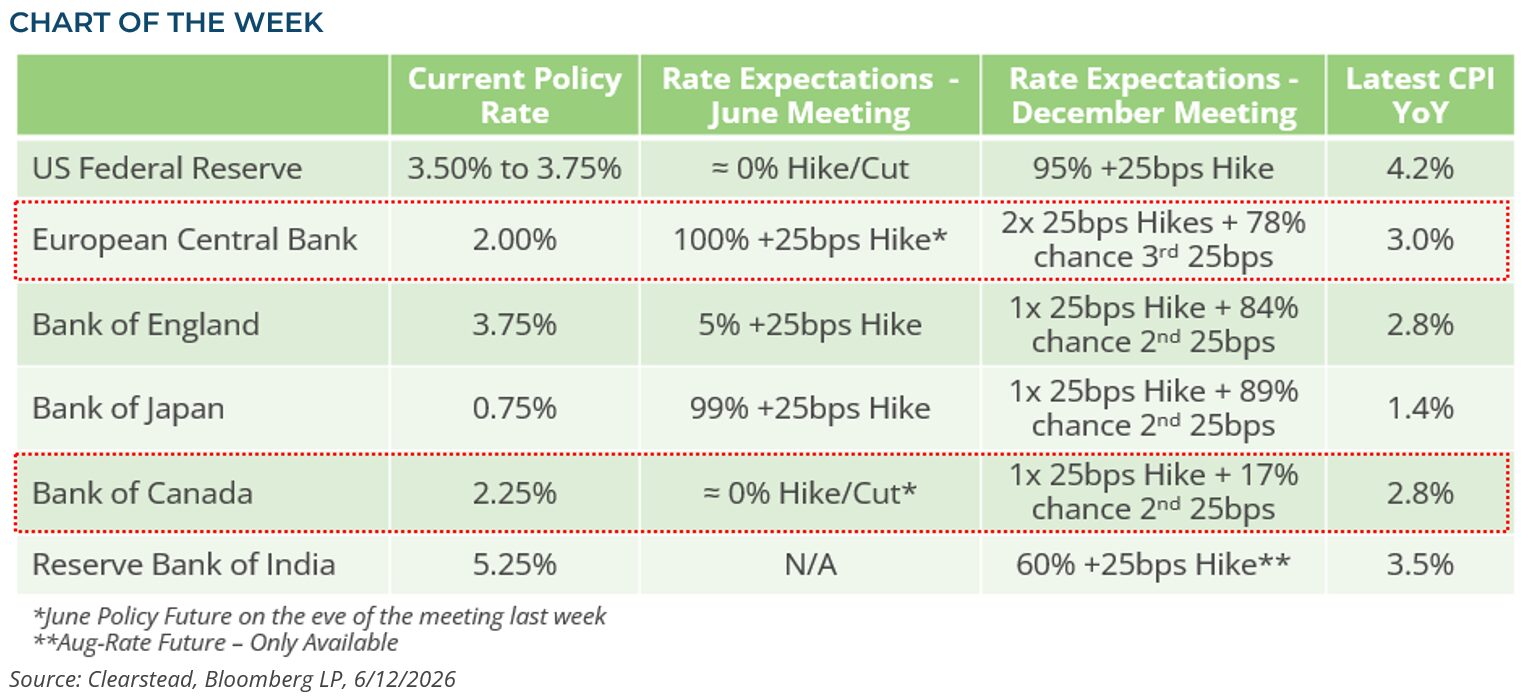

Inflation is a growing problem not only in the U.S. but around the world, and it is forcing global central banks to adopt a more hawkish stance. In the past few weeks, solid employment numbers (see RC 8-June) and rising inflation pressures in the US (see Observations above) have led markets to price in a 95% probability that the Fed will raise rates by at least 25 basis points by the end of the year—see Chart of the Week. Similarly, ahead of its meeting last week, markets had priced in a 100% probability that the European Central Bank (ECB) would hike its main policy rate by 25 basis points. Indeed, the ECB did just that, raising its policy rate to 2.25% and becoming the first G7 central bank to increase rates in response to mounting inflationary pressures, driven primarily by higher energy prices. Traders believe the ECB will deliver another 25-basis-point hike in the coming months, along with a 78% chance of a third 25-basis-point rate hike by December. In contrast, the Bank of Canada (BoC) held its main policy rate steady last week, as markets anticipated, but noted that “increases in energy prices and disruptions in global supply chains are weighing on global economic growth and pushing up inflation.” At present, markets have priced in at least one rate hike by the BoC before year-end, along with a 17% chance that the BoC will have to hike twice before then. Markets also expect the Bank of Japan (BoJ) to hike rates by 25 basis points when it meets this Tuesday, bringing its main policy rate to 1.0%, Japan’s highest rate since 1995. The U.S. Federal Reserve will also meet this week—its first meeting under new Fed Chairman Kevin Warsh—and markets expect the Fed to hold rates steady despite recent inflation data moving higher. Despite the global energy price surge that has spiked the cost for gasoline, jet fuel, and diesel, global economic activity has proven strikingly resilient, and this has led increasingly to global central banks moving towards tighter monetary policy and a greater possibility of higher global interest rates. This may ultimately pressure global growth as well as global equity returns. However, thus far, investors seem largely unfazed by the shift toward tighter monetary policy and higher rates. Much could change over the summer if the U.S.-Iran war moves toward a permanent and lasting ceasefire, which should work to relieve some inflationary pressures. However, the summer and fall could be volatile if the Strait of Hormuz remains closed and the prospect of higher rates becomes more firmly crystallized in the minds of global investors.

[1] Bloomberg LP, 6/12/2026

Information provided in this article is general in nature, is provided for informational purposes only, and should not be construed as investment advice. These materials do not constitute an offer or recommendation to buy or sell securities. The views expressed by the author are based upon the data available at the time the article was written. Any such views are subject to change at any time based on market or other conditions. Clearstead disclaims any liability for any direct or incidental loss incurred by applying any of the information in this article. All investment decisions must be evaluated as to whether it is consistent with your investment objectives, risk tolerance, and financial situation. You should consult with an investment professional before making any investment decision. Performance data shown represents past performance. Past performance is not an indicator of future results. Current performance data may be lower or higher than the performance data presented. Performance data is represented by indices, which cannot be invested in directly.

Related or Tagged New Posts

market perspectives

July 27th 2026

Research Corner | 7/27/2026

market perspectives

July 20th 2026

Research Corner | 7/20/2026

market perspectives

July 13th 2026

Research Corner | 7/13/2026

market perspectives

July 8th 2026

Quarterly Market Insights | 2Q26

market perspectives

July 6th 2026

Research Corner | 7/6/2026

market perspectives

June 29th 2026

Research Corner | 6/29/2026

market perspectives

June 22nd 2026

Research Corner | 6/22/2026

market perspectives

June 8th 2026

Research Corner 6/8/2026

market perspectives

June 1st 2026

Research Corner | 6/1/2026

market perspectives

May 26th 2026

Research Corner | 5/26/2026

market perspectives

May 18th 2026

Research Corner | 5/18/2026

market perspectives

May 11th 2026

Research Corner | 5/11/2026