OBSERVATIONS

- Markets were mixed last week with the S&P 500 losing 1.9%, while small caps (Russell 2000) gained 1.0% and the yield on the 10-Year Treasury fell 8 basis points to end the week at 4.37%.1

- New home sales fell to 580k (annualized rate), which was 7.3% below the April 2026 new home sales rate of 626k and is 6.8% below the rate of new home sales in May 2025.1

- The Architectural Billings Index—a leading index of broad non-residential construction activity—weakened further in May to 44.5 from April’s 48.3 figure indicating even more architectural firms are reporting a decline in billings than those reporting an increase. The index has been in contraction territory (<50) for 43 of the past 44 months.1

- The Fed’s preferred inflation gauge, the PCE price index, showed that headline prices increased in May by 4.1% year-over-year (YoY), while core-PCE, which removes food and energy, rose by 3.4% YoY. Both PCE and core PCE were in line with expectations, but elevated relative to April’s figures—3.8% YoY and 3.3% YoY respectively.1

- Durable goods fell by 4.5% month-over-month (MoM) in May largely due to a decline in aircraft orders which had surged in April, while durable goods orders ex-transportation increased by 1.3% MoM—both the headline figure and the ex-transportation figure were slightly better than expected.1

- Initial unemployment claims remain very low and registered only 215k last week, which was a 12k claim decrease from the week prior. Compared to the same week last year there were 20k fewer claims.1

EXPECTATIONS

- The ongoing US-Iran peace talks have allowed an increasing number of oil tankers to transit the Strait of Hormuz. As a result, oil prices have declined on both the spot and futures markets with WTI crude trading below $70 per barrel for the first time since the US-Iran conflict began in late February.1

- The final estimate for Q1 real GDP growth registered at 2.1% (annualized rate) and the Atlanta Fed’s GDPNow model currently indicates that Q2 real GDP is tracking towards 2.5%. Together these data points suggest a resilient US economy which is gradually picking up momentum.1

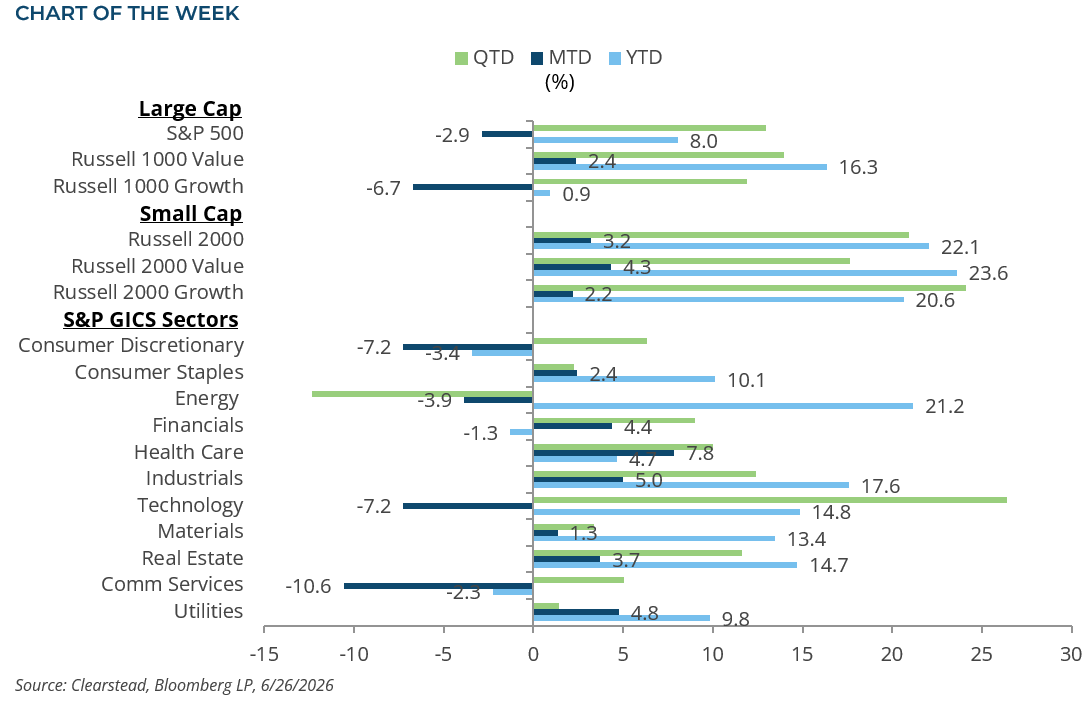

ONE MORE THOUGHT: June Shaping Up to be a Tougher Month for Equities1

With only two trading days left in the month (and the quarter), it is likely that June will mark a small reversal of the momentum in equities that marked April and May. As the US and Iran pivoted towards a shaky ceasefire in early April, equities began a significant rally. The S&P 500 gained over 10% in April and another 5% in May, marking one of the strongest two-month rallies since the end of WWII. However, after nine straight weeks of gains, equities fell in early June and are likely to end the month modestly lower than they started. However, while the S&P finished last week -2.9% lower month-to-date (MTD), small cap stocks (Russell 2000) have gained over 3.2% MTD and mid cap stocks (Russell Midcap) are up over 2.4%. There have also been marked differences in returns in June by style and sector. For instance, growth stocks (Russell 1000 Growth) gained nearly 20% between 1-April and 29-May but fell by 6.7% MTD in June. Whereas large cap value stocks (Russell 1000 Value) only gained about 11.4% during April and May but have tacked on another 2.4% gain MTD in June. For the quarter, large cap value stocks are likely to outpace their growth peers. In terms of sectors, Communication Services (-10.6%) and Consumer Discretionary (-7.3%) were the largest decliners for the month, but overall, seven of eleven sectors registered gains in June, led by Industrials which gained over 4.9% for the month. SpaceX, which went public on June 12th at $135 per share, initially rose to nearly $220 on its third trading day, but then declined to end the month at just over $153. Outside of the US, equities also broadly faced some tougher times. Both developed market equities (MSCI EAFE -0.97%) and emerging market equities (MSCI EM -2.4%) traded lower. The strengthening of the US dollar during the month also did not help these indices as a stronger dollar lowers foreign equities returns for US-based investors. Despite the negative return for global equities in June, equities are still poised to have a strong Q2. Q2 was marked by steadily moderating geopolitical risks, a resilient US economy, and strong corporate fundamentals that may persist throughout this summer and continue to provide some solace to investors.

[1] Bloomberg LP, 6/26/2026

Information provided in this article is general in nature, is provided for informational purposes only, and should not be construed as investment advice. These materials do not constitute an offer or recommendation to buy or sell securities. The views expressed by the author are based upon the data available at the time the article was written. Any such views are subject to change at any time based on market or other conditions. Clearstead disclaims any liability for any direct or incidental loss incurred by applying any of the information in this article. All investment decisions must be evaluated as to whether it is consistent with your investment objectives, risk tolerance, and financial situation. You should consult with an investment professional before making any investment decision. Performance data shown represents past performance. Past performance is not an indicator of future results. Current performance data may be lower or higher than the performance data presented. Performance data is represented by indices, which cannot be invested in directly.

Related or Tagged New Posts

market perspectives

August 7th 2026

July Review 2026

market perspectives

August 3rd 2026

Research Corner | 8/3/2026

market perspectives

July 27th 2026

Research Corner | 7/27/2026

market perspectives

July 20th 2026

Research Corner | 7/20/2026

market perspectives

July 13th 2026

Research Corner | 7/13/2026

market perspectives

July 8th 2026

Quarterly Market Insights | 2Q26

market perspectives

July 6th 2026

Research Corner | 7/6/2026

market perspectives

June 22nd 2026

Research Corner | 6/22/2026

market perspectives

June 15th 2026

Research Corner 6/15/2026

market perspectives

June 8th 2026

Research Corner 6/8/2026

market perspectives

June 1st 2026

Research Corner | 6/1/2026

market perspectives

May 26th 2026

Research Corner | 5/26/2026