OBSERVATIONS

- Markets traded higher last week extending the S&P 500’s winning streak to eight consecutive weeks. The S&P 500 gained 0.9%, small caps (Russell 2000) gained 2.8%,hp[ and the yield on the 10-year fell 3 basis points to end the week at 4.56%.[1]

- In May, the NAHB/Wells Fargo National Housing Market Index increased to 37 from April’s 34 reading, with small improvements in all three sub-components: current sales conditions, foot traffic at model homes, and expectations for future sales.[1]

- While housing starts were weak in April, they beat expectations. April delivered 1.465 million (annualized rate) new homes being built, 2.8% below March’s 1.507 million rate, driven by a 9% decline month-over-month in starts for single-family homes.[1]

- The Architectural Billings Index—a leading index of broad non-residential construction activity—declined from 49.8 in March to 48.3 in April, an indication that the share of architectural firms reporting a decline in billings was larger than those reporting an increase. The index has remained below 50 since January 2023, implying that most of the industry is seeing soft demand.[1]

- Initial unemployment claims remain low, registering 209k new claims last week—a fall of 3k claims from the week prior—and 15k fewer claims as compared to the same week last year. Through the first 20 weeks of the year, 2026 claims are the second fewest on record. Only 1969 had fewer claims in the first 20 weeks of the year.[1]

EXPECTATIONS

- Minutes from the most recent Fed meeting suggest a more hawkish policy bias: most officials indicated they would support higher rates if inflation remained persistently above 2%, and many favored removing language from the statement that implied a willingness to cut rates at upcoming meetings. That concern was underscored by the three Fed presidents who dissented because they viewed the statement as carrying an implicit easing bias.[1]

- Q1 earnings season has effectively wrapped up with 94% of the S&P 500 having reported, including NVIDIA. Earnings beats have been strong with 84% of firms beating estimates, above the 5-year (78%) and 10-year (76%) averages. Q1 earnings are up 28.4% year-over-year—the strongest quarter since Q4-2021.[2]

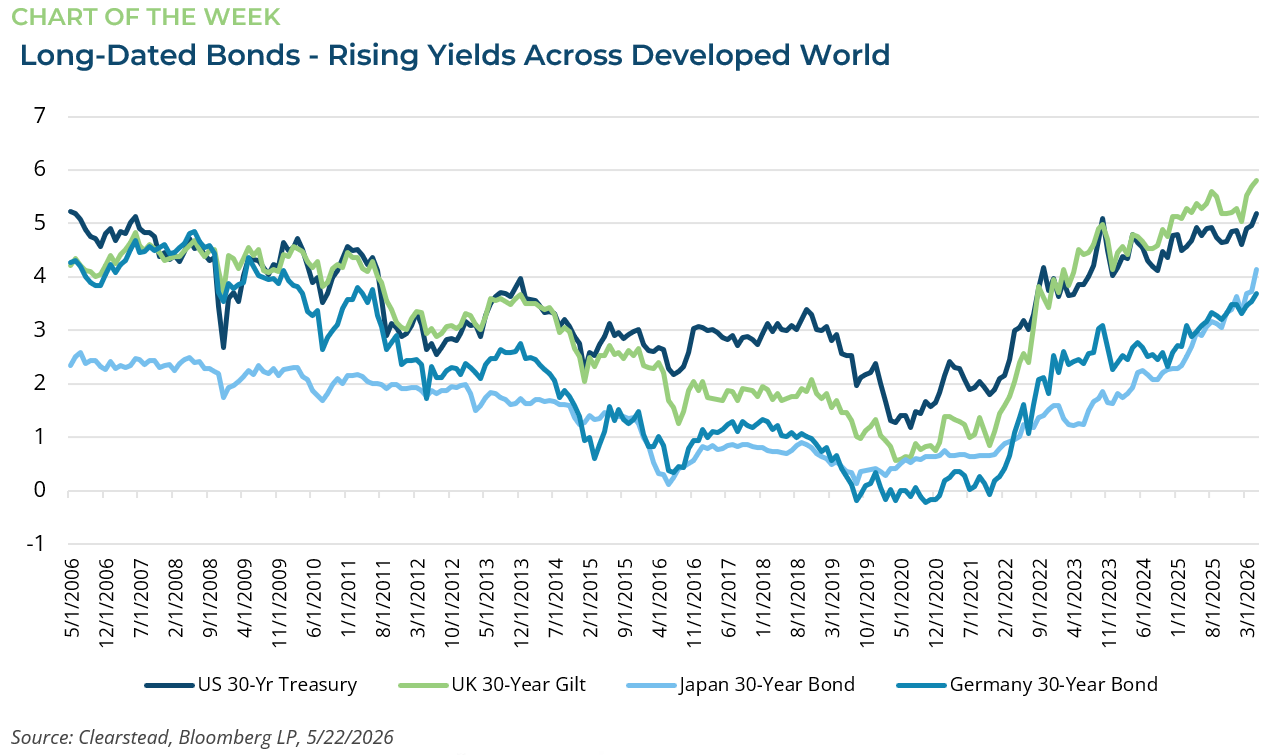

ONE MORE THOUGHT: Global Interest Rates Rise[1]

Interest rates have been volatile over the past few weeks. On Friday, May 8, the yield on the 10-year Treasury closed at 4.36%. By last Wednesday, it had risen to 4.67%—a 31-basis-point increase over eight trading days. The 30-year yield moved nearly as much during that period, climbing from 4.94% to 5.18%, its highest closing level since mid-2007. The rise in long-dated bond yields is not solely a U.S. phenomenon; yields on longer-dated bonds have been increasing across the developed world—see Chart of the Week. The reasons are multifaceted but share common themes. In most countries, inflation remains above central banks’ targets, government deficits are widening, and the U.S.-Iran war is exacerbating both issues. While the first two factors are well established, recent data suggests the inflation problem is worsening at the margin. Since early April, a fragile ceasefire in the U.S.-Iran war has held, but the risk of renewed fighting has increased in recent weeks. The result has been a repricing of expectations for future central bank action. In early April, Fed funds futures implied a 25% chance of a 25-basis-point rate cut by December 2026 and a better-than-50% chance of such a rate cut by mid-2027. By May 1, expectations had shifted, with no rate cuts priced in for the remainder of 2026 or the first half of 2027. As of last week, markets were pricing in an 80% chance of a 25-basis-point rate hike by December 2026 and a 40% chance of another rate hike by mid-2027. Late last week, U.S.-Iran talks appeared to be making progress, a few ships transited the Strait of Hormuz, and yields on longer-dated bonds eased from their midweek highs. However, inflation remains above the Fed’s 2% target and is proving harder to vanquish. While longer-term inflation expectations remain, in the Fed’s terminology, “well anchored,” there may be limits to the public’s patience. The further inflation drifts from the Fed’s target in the coming months, the more likely the Fed will need to act aggressively to prevent expectations from being reset at a structurally higher level. In addition, higher yields on longer-dated sovereign debt only worsen the challenges posed by profligate government spending. After decades of dormancy, the bond vigilantes, it seems, may be assembling.

[1] Bloomberg LP, 5/22/2026

[2] FactSet Earnings Insight 5/21/2026

Information provided in this article is general in nature, is provided for informational purposes only, and should not be construed as investment advice. These materials do not constitute an offer or recommendation to buy or sell securities. The views expressed by the author are based upon the data available at the time the article was written. Any such views are subject to change at any time based on market or other conditions. Clearstead disclaims any liability for any direct or incidental loss incurred by applying any of the information in this article. All investment decisions must be evaluated as to whether it is consistent with your investment objectives, risk tolerance, and financial situation. You should consult with an investment professional before making any investment decision. Performance data shown represents past performance. Past performance is not an indicator of future results. Current performance data may be lower or higher than the performance data presented. Performance data is represented by indices, which cannot be invested in directly.

Related or Tagged New Posts

market perspectives

July 27th 2026

Research Corner | 7/27/2026

market perspectives

July 20th 2026

Research Corner | 7/20/2026

market perspectives

July 13th 2026

Research Corner | 7/13/2026

market perspectives

July 8th 2026

Quarterly Market Insights | 2Q26

market perspectives

July 6th 2026

Research Corner | 7/6/2026

market perspectives

June 29th 2026

Research Corner | 6/29/2026

market perspectives

June 22nd 2026

Research Corner | 6/22/2026

market perspectives

June 15th 2026

Research Corner 6/15/2026

market perspectives

June 8th 2026

Research Corner 6/8/2026

market perspectives

June 1st 2026

Research Corner | 6/1/2026

market perspectives

May 18th 2026

Research Corner | 5/18/2026

market perspectives

May 11th 2026

Research Corner | 5/11/2026