OBSERVATIONS

- Markets were mixed last week amid renewed tensions in the Middle East. The S&P 500 rose 1.3%, and small caps (Russell 2000) fell 0.6%. The yield on the 10-year Treasury rose 8 basis points to end the week at 4.56%, and oil prices (West Texas Intermediate Crude or WTI) rose 4.0% to $71 per barrel.1

- The ISM services PMI reading fell to 54.0 in June, down slightly from May’s 54.5 reading, indicating that activity in the services sector of the economy continues to grow albeit at a slightly slower pace. A number above 50 denotes expanding economic activity. The employment sub-index increased to 51.2 from May’s 47.9 figure, indicating improvement in net hiring in the services sector.1

- The US trade deficit for goods and services widened by 42.2% to $77.6 billion in May 2026, the widest gap in 14 months. Imports increased 3.3% to a record $395.3 billion (driven by AI capital goods), while exports fell 3.2% to $317.7 billion. The widening trade balance will weigh on real GDP growth figures for Q2 as the trade deficit subtracts from official growth estimates.1

- Existing home sales fell 2.4% to 4.09 million (annualized rate) from May’s 4.19 million. However, as compared to June-2025, existing home sales grew by 2.8%—the third consecutive month of year-over-year (YoY) gains.1

- Registering 215k new claims last week, initial unemployment claims remain low. Compared to the same week last year, there were ~16k fewer claims.1

EXPECTATIONS

- Recent Fed minutes indicated that officials broadly agreed they would need to raise interest rates if inflation remained elevated this year. In addition, most officials noted that the risks to inflation were skewed to the upside and that persistently elevated inflation could begin to negatively affect inflation expectations.1

- Q2 earnings season kicks off next week with the major US banks reporting. Earnings are shaping up to be quite strong again, with consensus estimates pointing to a 23.3% YoY increase. In addition, we’ve seen the highest number of companies issuing positive guidance since Q3-2021, led by the Technology sector.2

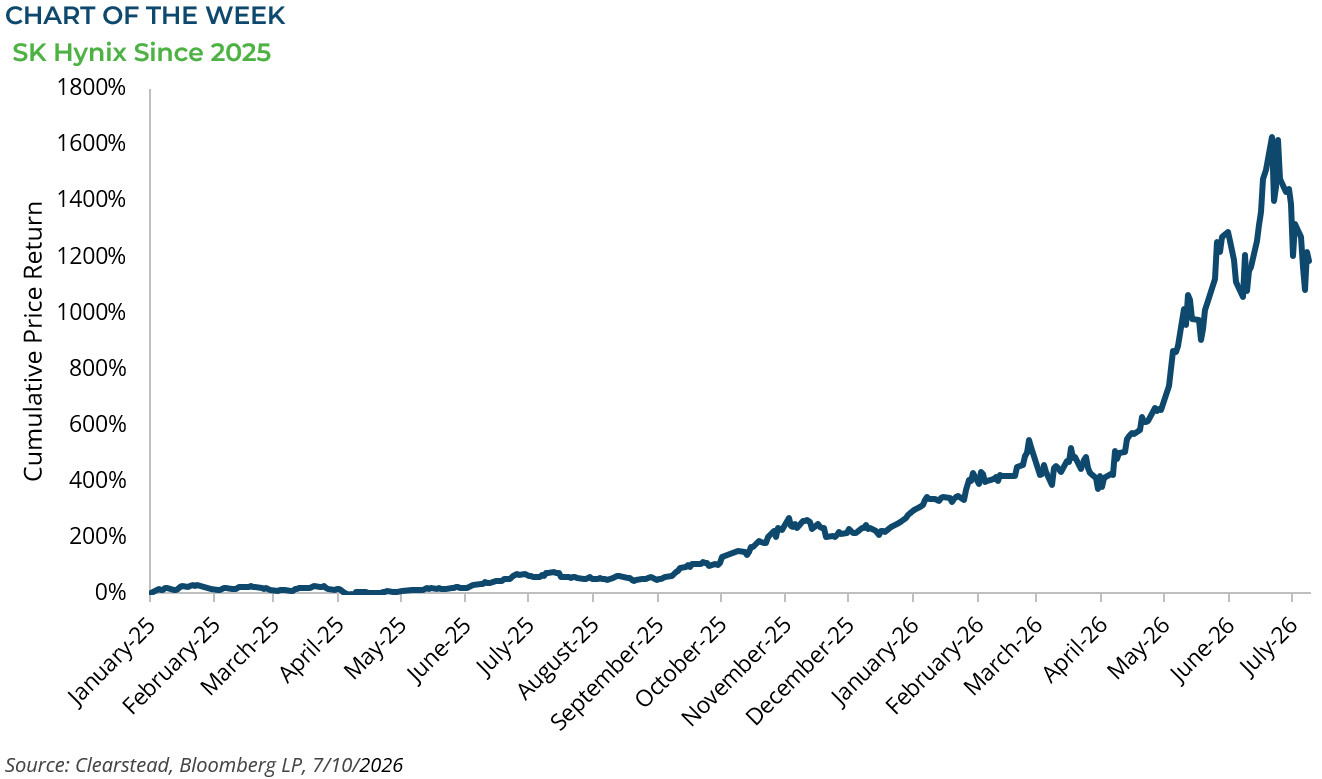

ONE MORE THOUGHT: SK Hynix Goes Public in the US1

SK Hynix began trading last week on the Nasdaq exchange under the ticker SKHY, with the initial offering at $149. SK Hynix is a Korean memory company that went public in 1996 on the Korean stock exchange. It originally traded as Hyundai Electronics before rebranding in 2012. The stock has soared over the past year, rising nearly 700%, as demand for its memory chips has surged from hyperscalers that use them in their datacenters. Hoping to capitalize on its current stock strength in Korea, the firm launched an equity offering for ADR shares in the United States. The offering raised about $27 billion for SK Hynix and was the largest-ever initial US stock sale by a foreign company, surpassing the IPOs of Alibaba and Saudi Aramco. The listing was oversubscribed ahead of pricing, drawing strong early demand from global long-only funds and technology-focused investors. The proceeds are earmarked for increasing infrastructure capacity rather than repairing the balance sheet. The stated rationale is a valuation gap. SK Hynix currently trades at a forward P/E of 6.2x versus its primary competitor Micron’s 7.0x, despite comparable exposure to the high-bandwidth memory boom. Korean policymakers hope a US-accessible ADR narrows that discount by unlocking a broader investor base. The listing arrived, however, just as Korean regulators were sounding the alarm that investor leverage has driven recent share price appreciation. South Korean retail margin debt reached a record 60 trillion won (≈$39 billion) at the end of May, and margin loans tied specifically to Samsung Electronics and SK Hynix jumped from roughly 2.5 trillion won (≈$1.7 billion) at the end of 2025 to over 9 trillion won (≈$6 billion). The risk is a forced liquidation cycle when prices reverse. Single-stock 2x levered ETFs tied to the two memory chipmakers, approved just three months ago, grew assets from about $3 billion at launch to $9 billion by mid-June, with 92% of holders being retail investors. The Bank of Korea has since warned that these ETFs, combined with record margin debt, could trigger a “volatility bomb.” Samsung and SK Hynix alone now account for more than 55% of KOSPI’s market cap and 63% of its trading volume. The SK Hynix ADR should, in theory, diversify the shareholder base and dilute some of the domestic concentration risk. However, in the near term, it lands on top of a Korean market where leverage, not fundamentals, is incrementally driving share prices. The success or failure of SK Hynix’s ADR listing, along with SpaceX’s recent trading trajectory, may also influence investor appetite for other AI-related IPOs later this year.

[1] Bloomberg LP, 7/10/2026

[2] https://insight.factset.com/record-high-number-of-sp-500-technology-companies-issuing-positive-eps-guidance-for-q2

Information provided in this article is general in nature, is provided for informational purposes only, and should not be construed as investment advice. These materials do not constitute an offer or recommendation to buy or sell securities. The views expressed by the author are based upon the data available at the time the article was written. Any such views are subject to change at any time based on market or other conditions. Clearstead disclaims any liability for any direct or incidental loss incurred by applying any of the information in this article. All investment decisions must be evaluated as to whether it is consistent with your investment objectives, risk tolerance, and financial situation. You should consult with an investment professional before making any investment decision. Performance data shown represents past performance. Past performance is not an indicator of future results. Current performance data may be lower or higher than the performance data presented. Performance data is represented by indices, which cannot be invested in directly.

Related or Tagged New Posts

market perspectives

August 3rd 2026

Research Corner | 8/3/2026

market perspectives

July 27th 2026

Research Corner | 7/27/2026

market perspectives

July 20th 2026

Research Corner | 7/20/2026

market perspectives

July 8th 2026

Quarterly Market Insights | 2Q26

market perspectives

July 6th 2026

Research Corner | 7/6/2026

market perspectives

June 29th 2026

Research Corner | 6/29/2026

market perspectives

June 22nd 2026

Research Corner | 6/22/2026

market perspectives

June 15th 2026

Research Corner 6/15/2026

market perspectives

June 8th 2026

Research Corner 6/8/2026

market perspectives

June 1st 2026

Research Corner | 6/1/2026

market perspectives

May 26th 2026

Research Corner | 5/26/2026

market perspectives

May 18th 2026

Research Corner | 5/18/2026